Facts and Figures

2023—Air Cargo Resilient Growth

The year 2023 marked a pivotal chapter for the air cargo industry, highlighting both opportunities and challenges shaped by global economic dynamics, geopolitical influences, and shifting consumer demands. Despite these complexities, the sector exhibited remarkable resilience, characterised by notable trends and regional variations in performance.

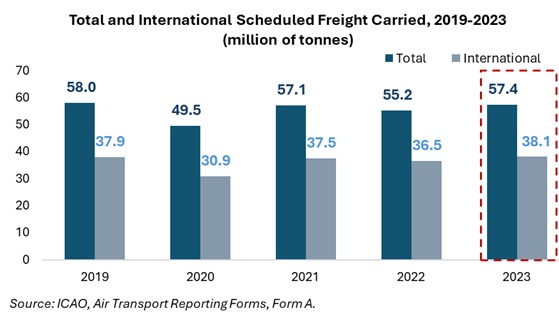

| In 2023, the total scheduled freight carried reached 57.4 million tonnes, reflecting a 4.0 per cent increase compared to 2022, thereby narrowing the gap with the pre-pandemic figure of 58.0 million tonnes recorded in 2019. Notably, international freight stood out, reaching 38.1 million tonnes, surpassing the 2019 pre-pandemic level of 37.9 million tonnes by 0.1 per cent. Remarkably the growth rate in comparison to 2022 was 4.3 per cent. |  |

The development of total non-scheduled freight in 2023 reached 14 million tonnes, representing a decline of 9.1 per cent compared to 2022, when it stood at 15.4 million tonnes. However, this figure remains 6.1 per cent higher than the pre-pandemic level of 10.5 million tonnes recorded in 2019. Notably, the share of non-scheduled services in total freight operations has increased significantly over the years. In 2019, non-scheduled services accounted for 15 per cent of total freight, whereas by 2023, this share had risen to approximately 20 per cent. This reflects an average annual growth rate of 5 per cent, highlighting the growing importance of non-scheduled services in meeting evolving air cargo demands, particularly in the context of e-commerce and supply chain disruptions.

The change of the share among scheduled and non-scheduled air cargo services may be because scheduled services may face constraints such as limited frequencies, fixed routes, or capacity shortages due to reduced passenger flights (especially during the pandemic) that ultimately result in less flexibility.

Non-scheduled services fill these gaps by providing dedicated capacity when scheduled services cannot meet demand. Correspondingly, total scheduled Freight Tonne-Kilometres (FTKs) amounted to approximately 223.8 billion, reflecting a growth rate of 2.7 per cent. International scheduled FTKs reached 194.5 billion, representing a 2.9 per cent increase compared to 2022. In terms of geographic traffic distribution, air carriers in the Asia Pacific region accounted approximately 38 per cent of scheduled international FTKs, followed by carriers in Europe with 25 per cent, the Middle East with 16 per cent, and North America with 14 per cent. Africa and Latin America and the Caribbean each contributed 3 per cent.

The Asia Pacific region emerged as the most dynamic player, achieving an impressive Total Scheduled FTK growth rate of 13.7 per cent, followed by the Middle East (+3.4%). In Asia Pacific region, this growth was primarily driven by Cathay Pacific (+39.8%), China Southern Airlines (+22.3%), and Air China (+30.6%). The Middle East region also recorded positive momentum, with a 3.4 per cent increase in Total Scheduled FTKs. The region benefited from its strategic role as a global logistics hub and the robust post-pandemic recovery of international services. The Middle Eastern carriers which pushing up the growth were Saudia (+65.3%), Oman Air (+92.6%), Kuwait Airways (+30.2%) and Emirates (+4.7%). Notably, Africa also demonstrated strong performance, recording 2.3 per cent growth, just below the aforementioned regions. This expansion was led by Ethiopian Airlines (+7.0%), Air Mauritius (+9.4%), and TAAG Angola (+17.2%). Furthermore, Africa's main international routes in 2023, based on growth rates, were Africa–Europe (+7.3%) and Africa–North America (+9.2%), with Belgium to/from Ethiopia emerging as the most significant country pair. This is consistent with the longstanding business relationship between Ethiopian Airlines and Liège Airport in Belgium.

In a press release issued by Ethiopian Airlines in Addis Ababa on 29 May 2024, the airline stated:

"The partnership between Ethiopian Cargo and Liege Airport has been mutually beneficial, contributing to the growth and development of both organisations. Ethiopian Cargo's extensive network and operational capabilities, combined with Liege Airport's modern infrastructure and efficient processes, have resulted in a highly effective and reliable cargo hub[1]."

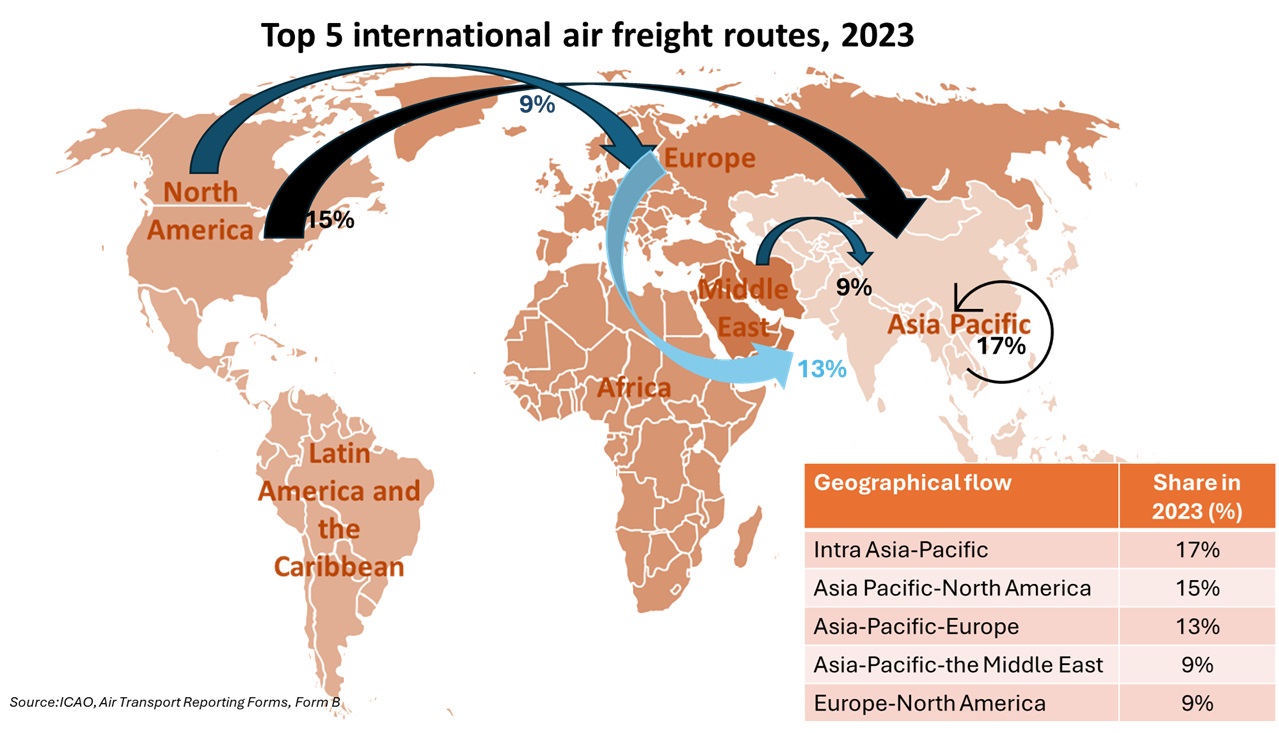

Based on Origin and Destination traffic reported and estimated by ICAO the main international air freight routes were in 2023:

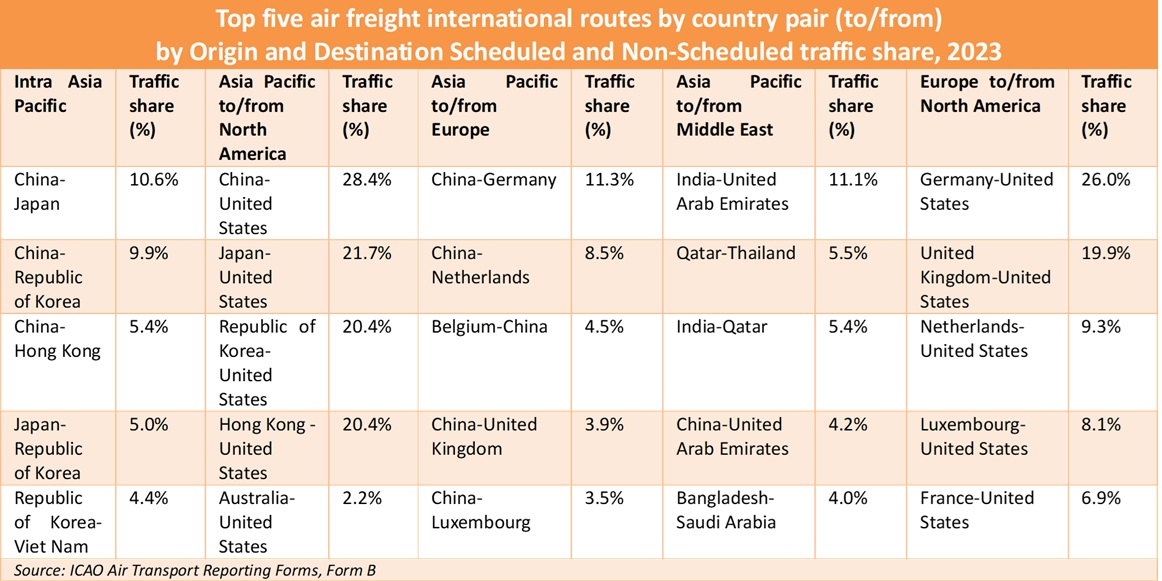

The top five international air freight routes in 2023 are intra-Asia Pacific, accounting for 17 per cent, followed by Asia Pacific to North America with 15 per cent, Asia Pacific to Europe with 13 per cent, Asia Pacific to Middle East with 9 per cent, and Europe to North America with 9 per cent. The following table shows the top five air freight international routes by country pair for 2023.

Non-Scheduled Freight Tonne-Kilometres: A Hidden Force in Air Cargo

In 2023, Total Non-Scheduled Freight Tonne-Kilometres (FTKs) reached 34.3 billion, reflecting a decline of 17.9 per cent compared to the previous year. Despite this drop, the figure remains 7.7 per cent higher than the pre-pandemic level of 23.7 billion FTKs recorded in 2019, underscoring the long-term resilience of non-scheduled air freight services. International Non-Scheduled FTKs followed a similar trend, totalling 25.7 billion in 2023—a year-on-year decrease of 21.4 per cent. However, compared to 2019, the average annual growth rate stood at 7.7 per cent, highlighting the sustained, long-term demand for these flexible services.

Notably, the geographic distribution of International Non-Scheduled FTKs differs significantly from that of scheduled services. Approximately 70 per cent of international non-scheduled cargo operations are concentrated in North America, followed by Europe at 19.5 per cent, and the Asia-Pacific region with 7.4 per cent. In stark contrast, Africa accounts for just 1.4 per cent, while the Middle East and Latin America and the Caribbean contribute 0.9 per cent and 0.7 per cent, respectively.

The prominence of non-scheduled services peaked during the pandemic years of 2020, 2021, and 2022, when widespread disruptions in global supply chains and reductions in passenger demand-driven, scheduled flight operations created an unprecedented demand for agile and rapid freight solutions. These services proved indispensable in ensuring the flow of essential goods, including medical supplies and e-commerce shipments, during a critical period. Their resilience throughout the pandemic further underscores their growing importance in the global air cargo industry, particularly in regions heavily reliant on flexible logistics solutions.

The Evolving Dynamics of Mail Tonne-Kilometres in Air Cargo

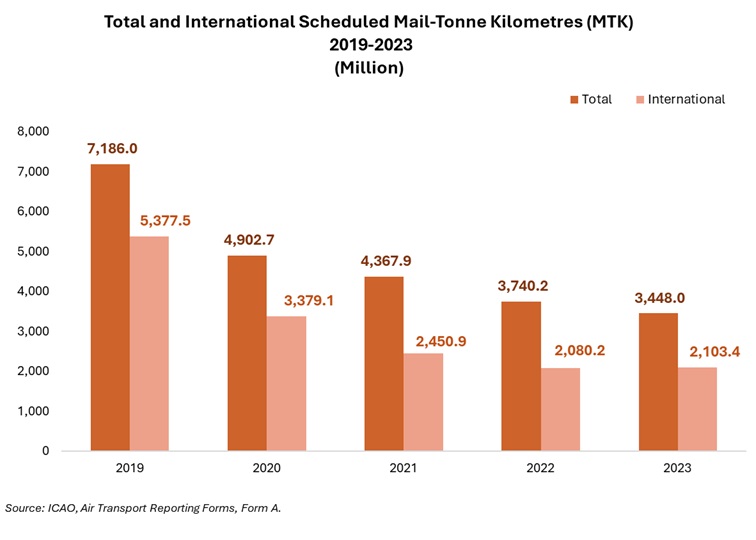

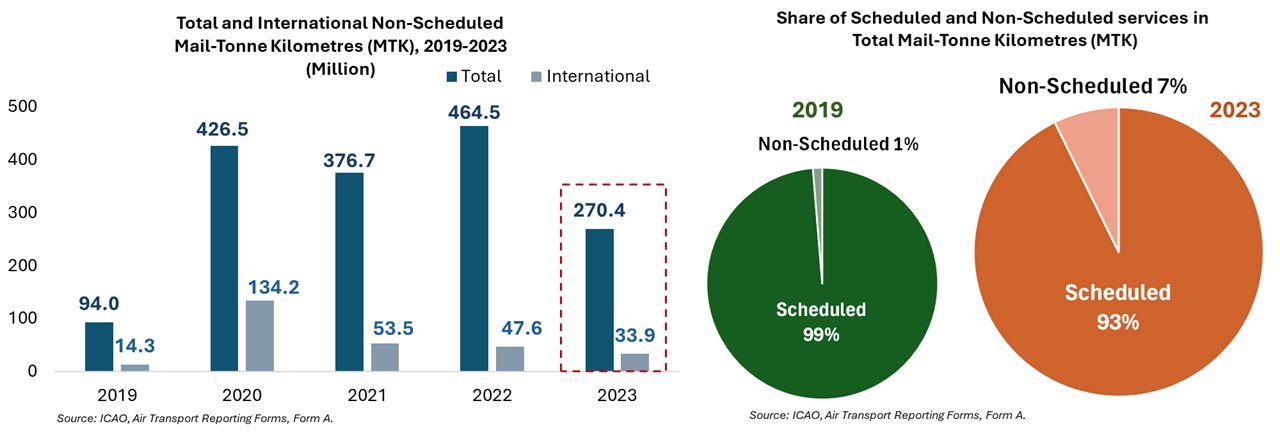

The evolution of Mail Tonne Kilometres (MTK) scheduled services highlights significant shifts in global air cargo dynamics, largely driven by the rapid growth of e-commerce. In 2023, the world's total MTK stood at 3,448 million, a decrease of 7.8 per cent compared to 2022. The 2023 figure falls significantly short of the pre-pandemic level in 2019, which was 7,186 million—approximately 50 per cent lower. However, the average annual growth rate 2023 vs 2019 is a decrease of 13.7 per cent.

| However, by 2023, International Scheduled MTK stood at 2,103.4 million with a modest 1.1 per cent growth in comparison to 2022, reflecting the gradual recovery of air cargo. In 2023, Total Mail Tonne Kilometres (MTK) performed by Non-Scheduled services amounted to 270.4 million, marking a substantial decline of 41.8 per cent compared to 2022. |

This downward trend was also evident in international non-scheduled services, which registered a negative growth rate of 28.8 per cent. The significant drop in 2023 can primarily be attributed to the underperformance of North American, Latin American, and African carriers.

It is worth noting that the distribution of Total Mail Tonne Kilometres (MTK) in Non-Scheduled services is heavily concentrated in North America, which accounts for approximately 57 per cent of the total. This is followed by Latin America and the Caribbean with 24 per cent, Europe with 14 per cent, the Asia Pacific region with 5 per cent, and Africa and the Middle East with less than 1 per cent.

However, it is noteworthy that Total and International Mail Tonne Kilometres for Non-Scheduled services have surpassed their pre-pandemic figures of 94 million and 14.3 million, respectively. This improvement corresponds to an average annual growth rate of 23.5 per cent for Total Mail Tonne Kilometres in Non-Scheduled services and 18.9 per cent for International Mail Tonne Kilometres in Non-Scheduled services.

This trend can be attributed to the inherent flexibility of non-scheduled services, often referred to as charter flights. Such services offer greater adaptability in terms of scheduling, routes, and capacity, enabling operators to swiftly respond to changes in demand. These include e-commerce surges, urgent deliveries, or postal requirements during periods of disruption to scheduled services.

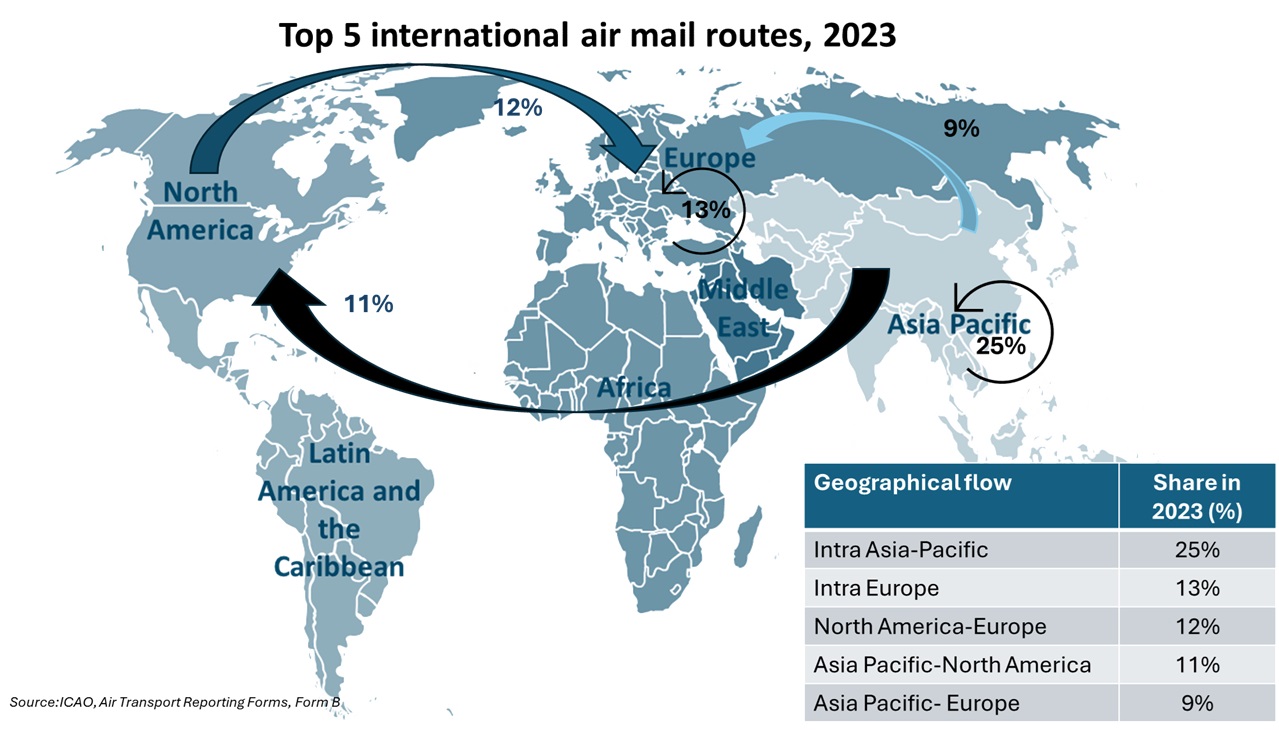

Based on Origin and Destination traffic reported and estimated by ICAO the main international air mail routes were in 2023:

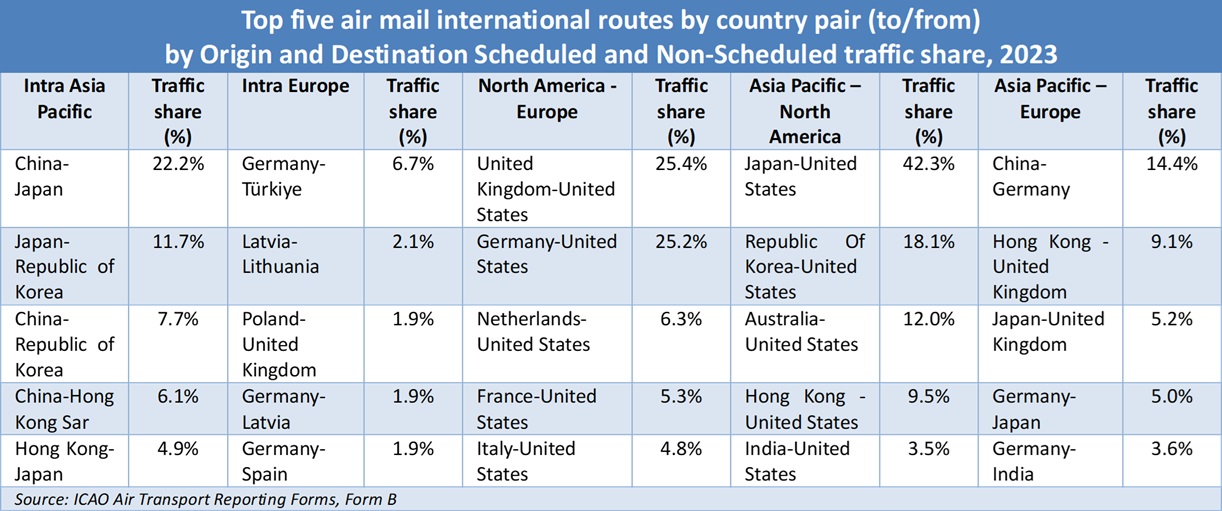

The top five international air mail routes in 2023 are intra-Asia Pacific, accounting for 25 per cent, followed by Intra Europe with 13 per cent, North America to Europe with 12 per cent, Asia Pacific to North America with 11 per cent, and Asia Pacific-Europe with 9 per cent. The following table shows the top five air mail international routes by country pair for 2023.

Air cargo capacity and load factors

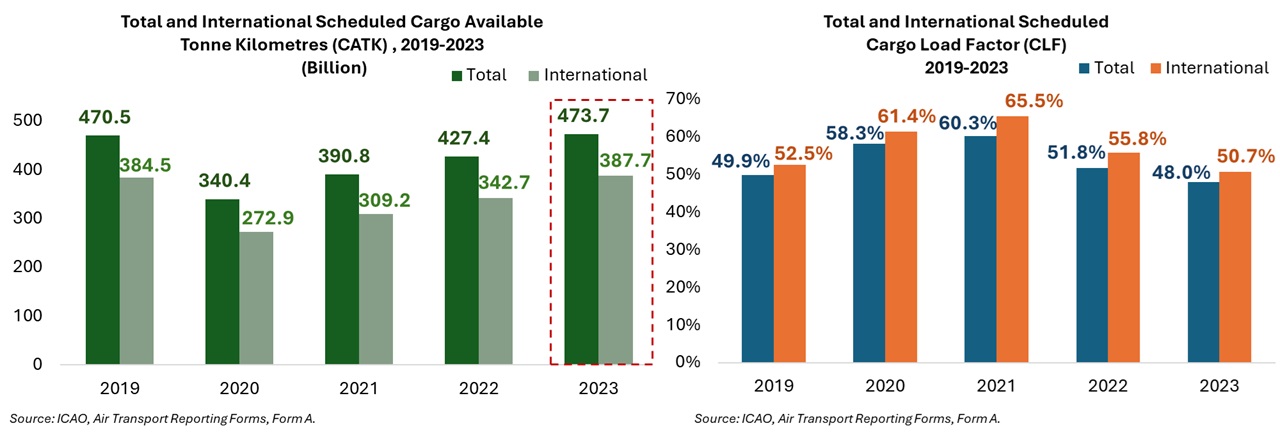

The Cargo Load Factor (CLF) in Total Scheduled services experienced a decline, dropping from 51.8 per cent in 2022 to 48.0 per cent in 2023, as capacity growth outpaced demand. For International Scheduled services, the cargo load factor fell by 9.1 percentage points, from 55.8 per cent in 2022 to 50.7 per cent in 2023. This trend highlights the industry's efforts to rebuild capacity while grappling with softer market conditions in certain regions. Total and International scheduled Cargo Available Tonne-Kilometres (CATK) reached 473.7 billion and 387.7 billion, respectively, marginally exceeding the pre-pandemic levels of 470.5 billion and 384.5 billion. Compared to 2022, total CATK increased by 10.8 per cent, while international CATK rose by 13.1 per cent.

On the other hand, Non-Scheduled services present a promising outlook. In 2023, Total Non-Scheduled Cargo Available Tonne-Kilometres (CATK) reached 78 billion, while International Non-Scheduled CATK stood at 56 billion. Both figures exceeded their pre-pandemic levels of 60 billion and 41.7 billion, respectively. This growth corresponds to an average annual increase of 5.4 per cent for Total Non-Scheduled CATK and 6.1 per cent for International Non-Scheduled CATK.

In 2023, the Cargo Load Factor for Total and International Non-Scheduled services stood at 44.3 per cent and 46.0 per cent, respectively, representing declines of 3.9 and 3.4 percentage points. Nevertheless, this should not be perceived as unfavourable. On the contrary, it may indicate an encouraging sign of capacity expansion, driven by increased demand for these services. This development aligns with the positive trajectory of the global economy and the sustained growth of cross-border trade in goods and services. This perspective is further reinforced by the fact that the 2023 cargo load factors exceeded the pre-pandemic levels of 39.7 per cent for Total Non-Scheduled cargo load factor and 42.6 per cent for International Non-Scheduled services. The average annual growth rate from 2019 to 2023 was 2.2 per cent for total Non-Scheduled cargo load factor and 1.6 per cent for International Non-Scheduled cargo load factor.

The performance of air cargo in 2023 was influenced by key factors:

- Economic Uncertainty: Global economic instability and geopolitical conflicts created significant challenges for the industry. These pressures were particularly evident in regions such as North America, where inflation dampened consumer spending. Conflicts and trade uncertainties in various parts of the world introduced both risks and opportunities, with some regions adapting more effectively than others to shifting trade flows.

- Capacity Expansion: The industry experienced a 10.8 per cent increase in overall capacity, primarily driven by international services, which grew by 13.1 per cent, while domestic services recorded a modest rise of 1.4 per cent. This expansion was enabled by the lifting of COVID-related lockdowns and crew quarantine restrictions, allowing airlines to restore freighter and passenger operations.

- E-commerce and Perishables: Strong demand for e-commerce and perishable goods provided a critical boost to the sector's growth.

In conclusion, 2023 highlighted the resilience of the air cargo industry amidst a dynamic global landscape. The combination of expanding capacity, robust international performance, and growing demand for specific goods underscores the sector's essential role in facilitating global trade and supporting economic recovery.