General

A Public-Private Partnership (PPP) is a partnership between the public sector and the private sector for the purpose of delivering a project or a service traditionally provided by the public sector. The advantage of a PPP is that the management skills and financial acumen of private businesses could create better value for money for taxpayers when proper cooperative arrangements between the public and private sectors are used.

PPP can increase the quality, the efficiency and the competitiveness of public services. It can supplement limited public sector capacities and raise additional finance in an environment of budgetary restrictions. The best use of private sector operational efficiencies can increase quality to the public and the ability to speed up infrastructure development.

When considering the commercialization or privatization of airports and air navigation services providers (ANSPs), States should bear in mind that they are ultimately responsible for safety, security and economic oversight of these entities (Doc 9082 - ICAO's Policies on Charges for Airports and Air Navigation Services - Section I, para. 6 refers).

Privatization should not in any way diminish the State’s requirement to fulfil its international obligations, notably those contained in the Chicago Convent ion, its Annexes and in air services agreements, and to observe ICAO’s policies on charges in Doc 9082 (Doc 9562 - Airport Economics Manual - para. 2.27 refers and Doc 9161 - Manual on Air Navigation Services Economics - para. 2.27 refers).

PPP Case Studies

The case studies have been prepared by the ICAO Secretariat based on material available (such as websites, reports, studies and the aviation press) and do not constitute an assessment or the expression of view by ICAO.

Airports

ANSPs

PPP - Airport Economics figures and analysis:

The following airport economics figures and analyses are extracted from the Airports Council International Policy Brief published in April 2017. More comprehensive and detailed airport economics figures and analyses are available in the ACI Airport Economics report and the policy brief.

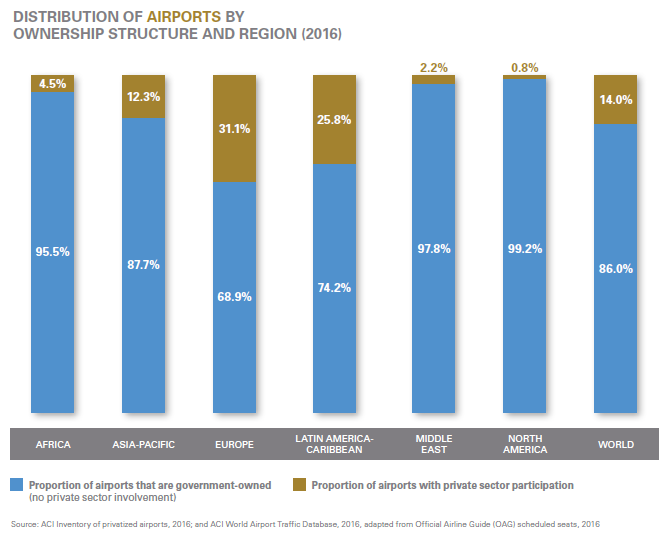

The following graph summarizes the percentage of airports in different regions of the world under different ownership models. As evident, by numbers the airports are mostly publicly owned. Government-owned operators or airports that are exclusively managed by public authorities continue to make up the lion’s share of airports across the globe, irrespective of the growing interest in private sector financing and management of the airports. An estimated majority (86%) of the 4,300 airports with scheduled traffic are public, in that they are owned by a government or governmental entity. Although airports with private sector participation account for an estimated 14% of airports worldwide, these airports handle over 40% of global traffic.

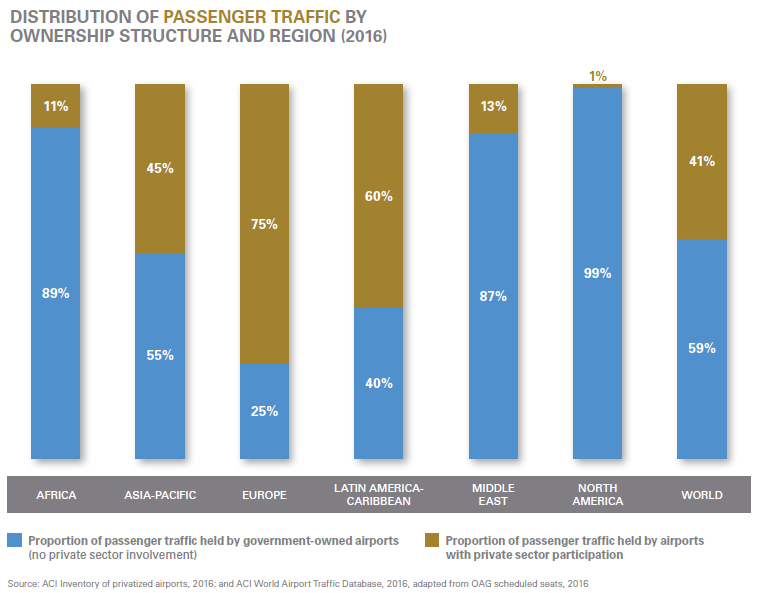

But if the distribution of passenger traffic is considered, as shown in the next graph, the growing involvement of private participation becomes explicit. 41% of global airport traffic is handled by airports that are managed and/or financed by private stakeholders. Private investments are essentially profit oriented, with a focus on good passenger service quality. Both these factors drive the private investors to the markets with greater traffic.

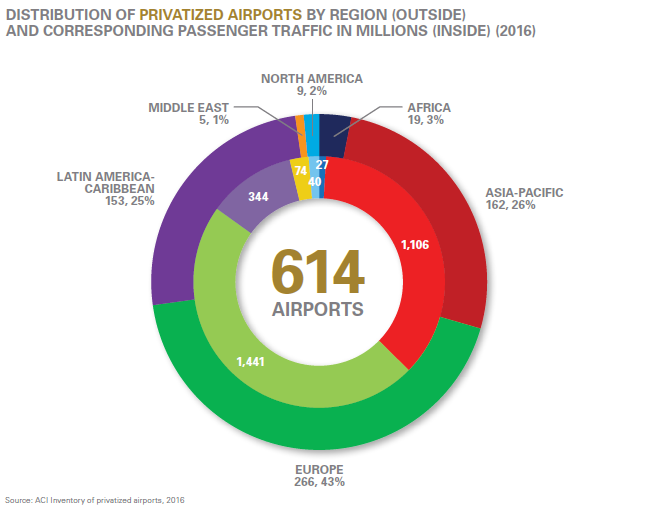

The figure below shows that out of the 614 airports as per the ACI Inventory of privatized airports, the highest number(266) exists in Europe, followed by Asia Pacific( 162). The figure also shows the corresponding passenger traffic in millions.

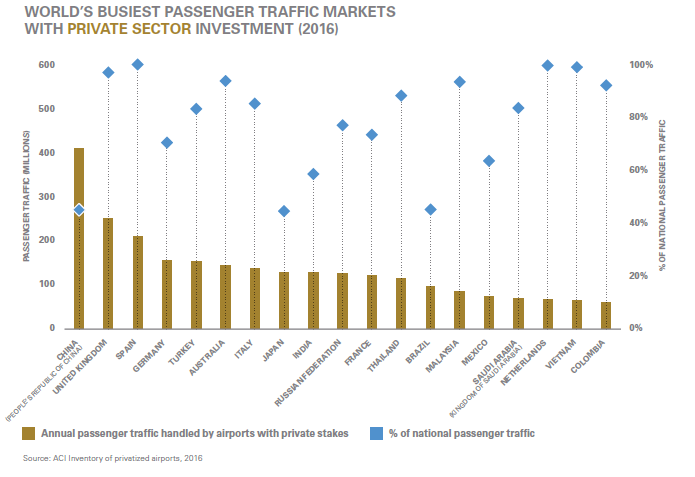

Finally, the graph below depicts the countries that are currently i.e. in 2016 the busiest markets by passenger traffic with the private sector investment. It shows relative passenger traffic proportions handled by airports that have private sector investment, compared to total traffic at the national level.