|

|

1. |

General questions about a market-based measure (MBM) and CORSIA |

|

none | 1 | ||||||||||||||||||||||||||||||||||||

| 1.1 | What is a market-based measure (MBM)? |

A market-based measure (MBM) is a policy tool that is designed to achieve environmental goals at a lower cost and in a more flexible manner than traditional regulatory measures. Examples of MBMs include levies, emissions trading systems, and carbon offsetting. |

table-row | 2 | |||||||||||||||||||||||||||||||||||||

| 1.2 | What is the contribution of aviation to global greenhouse gas emissions? |

Aviation (domestic and international) accounts for approximately 2 per cent of global CO₂ emissions produced by human activity, according to the information contained in relevant documents of the Intergovernmental Panel on Climate Change (IPCC), namely: IPCC Special Report on Aviation and the Global Atmosphere (p. 6); IPCC AR4 Climate Change 2007: Mitigation of Climate Change (p.49); and IPCC AR6 Climate Change 2022: Mitigation of Climate Change (p.1086). In 2018, approximately 65 per cent of global aviation fuel consumption was from international aviation (see ICAO 2022 Environmental Report, p.24); applying this share to CO₂ emissions, international aviation is responsible for approximately 1.3 per cent of global CO₂ emissions.

|

table-row | 3 | |||||||||||||||||||||||||||||||||||||

| 1.3 | Why does the Paris Agreement not include international aviation emissions? |

The Paris Agreement under the United Nations Framework Convention on Climate Change (UNFCCC) is an international treaty that was agreed in December 2015 and entered into force in November 2016 to enhance the implementation of the UNFCCC. Its aim is “to strengthen the global response to the threat of climate change” by establishing specific goals for “holding the increase in the global average temperature to well below 2°C above pre-industrial levels and pursuing efforts to limit the temperature increase to 1.5°C”.

The Paris Agreement, adopted under the UNFCCC, addresses sectors and related greenhouse gas emissions following an approach similar to that of its overarching Convention. Specifically, governments working under the auspices of the UNFCCC have agreed that while all domestic GHG emissions are dealt with under the UNFCCC, GHG emissions associated with international aviation and maritime transport are to be dealt with under ICAO and International Maritime Organization (IMO), respectively. This approach is consistent with similar UNFCCC decisions that also apply to the Kyoto Protocol.

In this regard, GHG emissions from domestic aviation, as per other domestic sources, are calculated as part of the UNFCCC national GHG inventories and are included in national totals (part of the Nationally Determined Contributions (NDCs) of the Paris Agreement), while GHG emissions from international aviation are reported separately and are not included in NDCs.

ICAO, as a specialized UN agency to address all matters related to international civil aviation, including environmental protection, has been diligently addressing GHG emissions from international aviation. The ICAO agreement on carbon neutral growth and CORSIA complements the ambition of the Paris Agreement and constitutes the most significant international climate-related agreement since its adoption.

|

table-row | 5 | |||||||||||||||||||||||||||||||||||||

| 1.4 | Why did ICAO decide to develop a global MBM scheme for international aviation? |

The ICAO Assembly has resolved that ICAO and its Member States, with relevant organizations, would work together to strive to achieve a collective medium term global aspirational goal of keeping the global net CO₂ emissions from international aviation from 2020 at the same level (so-called "carbon neutral growth from 2020").

The Assembly also defined a basket of measures designed to help achieve the ICAO's global aspirational goal. This basket includes aircraft technologies such as lighter airframes, higher engine performance and new certification standards, operational improvements (e.g., improved ground operations and air traffic management), sustainable aviation fuels, and market-based measures (MBMs).

Based on the environmental trend assessment by the ICAO Council's Committee on Aviation Environmental Protection (CAEP), international aviation fuel consumption is estimated to grow by between 1.9 and 2.6 times by 2050 compared to the 2018 levels, depending on the technology and Air Traffic Management scenario considered (for further details on the CAEP assessment, please refer to Assembly Working Paper A41-WP/93 presented to the 41th Session of the ICAO Assembly). Comparing with the previous CO₂ trends, the current assessment shows in 2040 approximately 15% lower CO₂ emissions for the base scenario with technology freeze and no operational improvements.

The aggregate environmental benefits achieved by non-MBMs measures will not be sufficient for the international aviation sector to reach its aspirational goal. According to the CAEP analysis, international aviation emissions are forecasted to grow in the coming decades, as the projected annual improvements in aircraft fuel efficiency of around 1 to 2 per cent (as result of technological and operational measures), and the reductions from the use of sustainable aviation fuels in the short- to medium-term are expected to be largely surpassed by the forecasted traffic growth of around 5 per cent per year.

A global MBM scheme can help fill the emissions reductions gap, while further advancements in key technologies (e.g., engines, fuels) may result in further CO₂ emissions reductions in the future. The global MBM scheme is the preferred approach compared to having a patchwork of regional and local measures.

The Figure below illustrates the estimated contribution of CORSIA for reducing international aviation CO₂ emissions.

|

table-row | 4 | |||||||||||||||||||||||||||||||||||||

| 1.5 | What ICAO process was followed to develop CORSIA? |

Discussions on the application of MBMs as a means to limit or reduce CO₂ emissions from international civil aviation had taken place prior to the 37th Session of the Assembly in 2010, which adopted Assembly Resolution A37-19: Consolidated statement of continuing ICAO policies and practices related to environmental protection — Climate change. Assembly Resolution A37-19 requested the Council, with the support of Member States and international organizations, to continue to explore the feasibility of a global MBM scheme by undertaking further studies on the technical aspects, environmental benefits, economic impacts and the modalities of such a scheme, taking into account the outcome of the negotiations under the United Nations Framework Convention on Climate Change (UNFCCC) and other international developments, as appropriate, and report the progress for consideration by the 38th Session of the ICAO Assembly in 2013.

The 37th Session of the Assembly also adopted global aspirational goals for the international aviation sector of annual average fuel efficiency improvement of 2 per cent, and keeping the global net carbon emissions from 2020 at the same level (also referred to as carbon neutral growth from 2020).

The work requested by Resolution A37-19 focused on the qualitative and quantitative assessments of potential options for a global MBM scheme for international aviation. Building on this work, the 38th Session of the ICAO Assembly in 2013, through Resolution A38-18: Consolidated statement of continuing ICAO policies and practices related to environmental protection — Climate change, decided to develop a global MBM scheme for international aviation, and requested the Council, with the support of Member States, to finalize the work on the technical aspects, environmental and economic impacts and modalities of the possible options for a global MBM scheme, including on its feasibility and practicability, taking into account the need for development of international aviation, the proposal of the aviation industry and other international developments, as appropriate, and without prejudice to the negotiations under the UNFCCC.

Assembly Resolution A38-18 further requested the Council to identify the major issues and problems, including those for Member States, and make a recommendation on a global MBM scheme that appropriately addresses them and key design elements, including a means to take into account special circumstances and respective capabilities of ICAO Member States. The Council was also requested to identify the mechanisms for the implementation of the scheme from 2020 as part of a basket of measures that also include technologies, operational improvements and sustainable aviation fuels to achieve ICAO’s global aspirational goals.

Following the 38th Session of the Assembly, the 200th Session of the Council in November 2013 supported that the Committee on Aviation Environmental Protection (CAEP) would continue to undertake technical tasks related to the development of a global MBM scheme, as requested by Resolution A38-18. The Council also decided upon the establishment of an Environment Advisory Group of the Council (EAG), which was mandated to oversee all the work related to the development of a global MBM scheme and make recommendations to the Council.

The EAG focused its work on a mandatory carbon offsetting approach as the basis for a global MBM scheme for international aviation. The EAG/15 meeting in January 2016 considered a draft Assembly Resolution text on a global MBM scheme, which was further refined throughout 2016 by two meetings of a High-level Group on a Global MBM Scheme in February and April 2016, a High-level Meeting on a Global MBM Scheme in May 2016 and a Friends of the President Informal Meeting in August 2016.

The Assembly, by adopting Resolution A39-3, agreed to implement a global MBM scheme in the form of CORSIA. It also requested the Council, with the technical contribution of CAEP, to develop the SARPs and related guidance material for the implementation of the Monitoring, Reporting and Verification (MRV) system under the CORSIA.

The CAEP developed SARPs for the CORSIA and, after amendment following the consultation with the Member States, the first edition of Annex 16, Volume IV was adopted by the Council at its 214th Session (11 – 29 June 2018), and became applicable on 1 January 2019.

The Assembly, at its 40th Session in 2019, acknowledged the progress made by ICAO and its Member States in taking the necessary steps towards implementation of CORSIA, and established a series of requests to the Council in order to ensure that CORSIA implementation would continue to be on track. This was reflected in the adoption of Assembly Resolution A40-19, which superseded Resolution A39-3.

The 41st Session of the ICAO Assembly (27 September – 7 October 2022) adopted Resolution A41-22 (Consolidated statement of continuing ICAO policies and practices related to environmental protection - Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA)), which superceeds Resolution A40-19.

The Council, at its 228th Session (13 – 31 March 2023), adopted Amendment 1 to Annex 16, Volume IV, resulting from proposed amendments by CAEP and from the outcome of the 2022 CORSIA periodic review. The resulting second edition of Annex 16, Volume IV became applicable on 1 January 2024.

|

table-row | 6 | |||||||||||||||||||||||||||||||||||||

| 1.6 |

What is CORSIA and how does it work, in general? |

The CORSIA has been adopted as complementary to the broader package of measures to help ICAO achieve its aspirational goal of carbon-neutral growth from 2020 onwards. CORSIA relies on the use of eligible emissions units from the carbon market to offset the amount of CO₂ emissions that cannot be reduced through the use of technological and operational improvements, and CORSIA eligible fuels.

The approach for CORSIA is based on comparing the total CO₂ emissions for a year (from 2021 onwards) against a baseline level of CO₂ emissions.

The ICAO Assembly, having considered the recommendations from the Council arising from the 2022 CORSIA periodic review (see question 2.28), adopted Resolution A41-22, which establishes adjustments to the definition of the CORSIA baseline as follows (Assembly Resolution A41-22, paragraph 11 b)):

See question 2.17 for more details on CORSIA’s baseline.

For any year from 2021 onwards, the international aviation CO₂ emissions covered by CORSIA that exceed the baseline level represent the sector's offsetting requirements for that year (see graph below for an illustrative example for a future year 20XX).

The sectoral offsetting requirements are shared among aeroplane operators covered under CORSIA based on the sector's growth factor and the individual CO₂ emissions of the operators. For more details on calculating offsetting requirements, please see question 2.15.

CORSIA will be implemented in three phases, as follows:

It is important to note that all States whose aeroplane operator undertakes international flights need to develop a monitoring, reporting and verification (MRV) system for CO₂ emissions from international flights starting from 1 January 2019. The requirement to monitor, report and verify CO₂ emissions from international aviation is independent from the offsetting requirements, and the data reported by States will be used for the calculation of the CORSIA's baseline, as well as for the basis of calculating aeroplane operators offsetting requirements, where applicable. See section 3 of these FAQs for more information on CORSIA MRV system.

|

table-row | 7 | |||||||||||||||||||||||||||||||||||||

| 2. | Questions about CORSIA’s key design elements | none | 8 | ||||||||||||||||||||||||||||||||||||||

| Key design element 1: Phased implementation of CORSIA |

|

none | |||||||||||||||||||||||||||||||||||||||

| 2.1 | What is the rationale for the phased implementation of CORSIA? |

Paragraph 9 of the Assembly Resolution A41-22 determines the phased implementation of the CORSIA, and the participation of States in the CORSIA offsetting. According to this paragraph, phased implementation of CORSIA intends to accommodate “the special circumstances and respective capabilities of States, in particular developing States, while minimizing market distortion.”

|

table-row | 9 | |||||||||||||||||||||||||||||||||||||

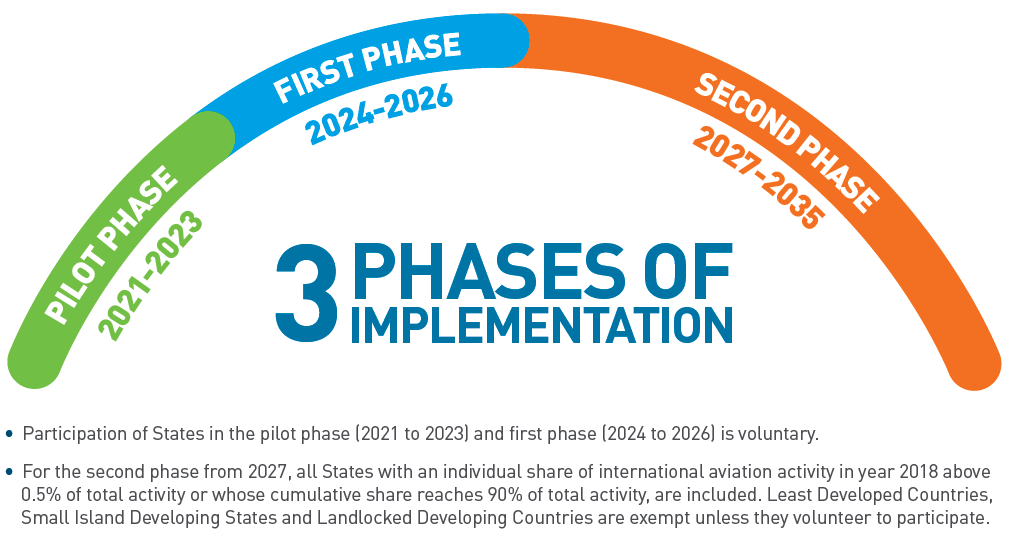

| 2.2 | What are the different phases? |

The CORSIA has three phases: a pilot phase (2021 – 2023); a first phase (2024 – 2026); and a second phase (2027 – 2035).

The difference between the phases is that the participation of States in the CORSIA offsetting in the pilot phase and in the first phase is voluntary, whereas the second phase is determined using criteria that are based on the 2018 RTK data and voluntary participation (See also questions 2.3 and 2.4 for details).

States that voluntarily decide to participate in CORSIA offsetting may join the scheme from the beginning of a given year, and should notify ICAO of their decision to join by June 30 of the preceding year.

The figure below illustrates the different phases of CORSIA.

|

table-row | 10 | |||||||||||||||||||||||||||||||||||||

| 2.3 | What is the difference between the pilot phase (from 2021 through 2023) and the first phase (from 2024 through 2026)? |

The requirements for the two phases are identical except for how the aeroplane operator’s offsetting requirements are determined by the State. Specifically:

• For the first phase, the calculation to determine an aeroplane operator’s offsetting requirements is based on the emissions in a given year (i.e. 2024, 2025 and 2026). |

table-row | 11 | |||||||||||||||||||||||||||||||||||||

| 2.4 | Which criteria determine the participation or exemption of States from CORSIA offsetting in its second phase from 2027 to 2035? |

Unlike the voluntary participation of States in the CORSIA offsetting in the pilot and first phases from 2021 to 2026, the second phase of the CORSIA from 2027 to 2035 applies to all Member States. There are, however, two categories of exemptions based on aviation-related and socio-economic criteria. These criteria for the exemption of States from the CORSIA offsetting requirements in the second phase are defined in A41-22 paragraph 9 e).

For aviation-related criteria, there are two thresholds:

|

table-row | 12 | |||||||||||||||||||||||||||||||||||||

| 2.5 | What is a “RTK”? |

Revenue Tonne Kilometers or RTKs is the utilised (or sold) capacity for passengers and cargo expressed in metric tonnes, multiplied by the distance flown. In other words the RTK levels correspond to the volume of air transport activity. As an aeroplane operator carries more passengers and cargo over a longer distance, the RTK levels of the operator increase.

A State’s RTK represents the total RTK levels of all aeroplane operators registered to that State. Annual RTK data is being reported from Member States to ICAO as part of the ICAO Statistics Programme, and published in the Annual Report of the ICAO Council.

RTK data for the year 2018 will be used for the purposes of determining the participation of States in the second phase of the CORSIA (see question 2.4).

|

table-row | 13 | |||||||||||||||||||||||||||||||||||||

| 2.6 | How are RTK shares calculated? |

A State’s individual RTK share is calculated by dividing the State’s RTKs by the total RTKs of all States.

The cumulative RTK share is calculated by sorting the individual RTK shares from the highest to lowest, then successively increasing the value by summing the RTK shares from highest to lowest until the value reaches 90%. The values of all States are considered for this calculation, regardless of whether a State is exempted or not from offsetting requirements under the CORSIA.

|

table-row | 14 | |||||||||||||||||||||||||||||||||||||

| Key design element 2: Route-based approach of CORSIA | none | ||||||||||||||||||||||||||||||||||||||||

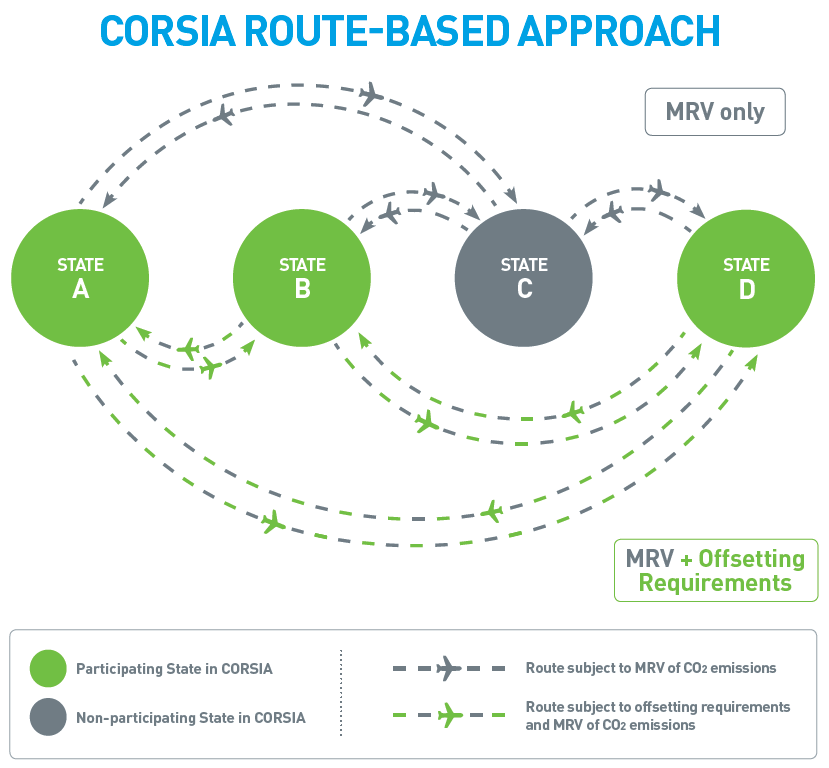

| 2.7 | What is the route-based approach of CORSIA? |

Paragraph 10 of the Assembly Resolution A41-22 defines the coverage of the CORSIA offsetting on the basis of routes between States, with a view to minimizing market distortions between aeroplane operators on the same routes. For this purpose, the approach is to provide equal treatment of all aeroplane operators on a given route. Specifically:

|

table-row | 15 | |||||||||||||||||||||||||||||||||||||

| 2.8 | What does “participation of States to CORSIA offsetting” mean for the route-based approach? |

The term “participation of States to CORSIA offsetting” means that if a State participates in CORSIA offsetting, then all routes between this State and all other States participating in CORSIA offsetting are covered by offsetting requirements.

Please see questions 2.2 and 2.4 for details on how the participation to CORSIA offsetting is being determined in different phases.

|

table-row | 16 | |||||||||||||||||||||||||||||||||||||

| 2.9 | Can the characterisation of a route as “covered” or “not covered” by the CORSIA offsetting change over time? |

Paragraph 10 of the Assembly Resolution A41-22 determines the characterisation of a route as “covered” or “not covered” by the CORSIA offsetting requirements, on the basis of whether the States connecting the route participate in CORSIA offsetting.

The voluntary participation of States in different phases of the CORSIA will determine the overall coverage of the scheme.

To give certainty on the routes to be covered by the CORSIA offsetting requirements every year, the Assembly Resolution A41-22 sets a deadline by 30 June of the preceding year for States to notify ICAO of their intention to voluntarily participate in the scheme, or discontinue their participation, from 1 January of the following year.

|

table-row | 17 | |||||||||||||||||||||||||||||||||||||

| 2.10 | Do States and aeroplane operators that do not participate in the CORSIA offsetting have any requirements under CORSIA? |

The CORSIA MRV requirements are applicable to all aeroplane operators that produce annual CO₂ emissions greater than 10 000 tonnes from the use of aeroplane(s) with a maximum certificated take-off mass greater than 5 700 kg conducting international flights. The requirement to monitor, report and verify CO₂ emissions from international aviation is thus independent from the generation of offsetting requirements, and applies to the said aeroplane operators from 1 January 2019.

From the start of CORSIA's pilot phase on 1 January 2021, all international flights between two States not participating in CORSIA for offsetting purposes are exempted from the offsetting requirements of CORSIA, while retaining simplified reporting requirements. The same applies to international flights between a State participating in CORSIA for offsetting purposes and another State not participating in CORSIA for offsetting purposes (Assembly Resolution A41-22, paragraph 10).

|

table-row | 18 | |||||||||||||||||||||||||||||||||||||

| 2.11 | Can an aeroplane operator have offsetting requirements, even if its State of registration does not participate in CORSIA offsetting? |

Yes. Because of the CORSIA’s route-based approach, an operator operating on routes between participating States would be subject to the offsetting requirements under the CORSIA, no matter whether its State of registration participates in CORSIA offsetting or not.

|

table-row | 140 | |||||||||||||||||||||||||||||||||||||

| 2.12 | What would happen to the CORSIA emissions coverage if an operator of a non-participating State flies on the routes between participating States (e.g. fifth-freedom traffic right)? |

Because of the CORSIA’s route-based approach, these routes between participating States would be subject to the coverage of emissions offsetting requirements under the CORSIA. Thus, an operator of a non-participating State would be subject to offsetting requirements if it had a flight between two participating States, and emissions from such flights would be added to the coverage of CORSIA’s offsetting requirements.

|

table-row | 19 | |||||||||||||||||||||||||||||||||||||

| 2.13 | What would happen to the CORSIA emissions coverage if a State without an operator undertaking international flights decides to participate in the CORSIA offsetting? |

States without an operator flying international flights are encouraged to participate in all phases of the CORSIA. If such a State decides to participate, international flights to and from that State to other participating States are additionally included for the CORSIA’s offsetting requirements, due to the route-based approach. The total international emissions covered by CORSIA offsetting would ultimately increase.

|

table-row | 20 | |||||||||||||||||||||||||||||||||||||

| Key design element 3: CORSIA offsetting requirements and eligible emissions units | none | ||||||||||||||||||||||||||||||||||||||||

| 2.14 | What is offsetting and how does it work, in general? |

In general, offsetting is done through the purchase and cancellation of emissions units (see question 4.24), arising from different sources of emissions reductions achieved through mechanisms, programmes or projects. The buying and selling of eligible emissions units happens through the carbon market. The price of the emissions units in the carbon market is influenced by the law of supply (availability of emissions units) and demand (level of offsetting requirements).

“Cancelling” means the permanent removal and single use of an emissions unit so that the same emissions unit cannot be used more than once. This is done after an aeroplane operator has purchased emissions units from the carbon market. For CORSIA, an aeroplane operator is required to meet its offsetting requirements by cancelling CORSIA Eligible Emissions Units in a quantity equal to its total final offsetting requirements for a given compliance period. CORSIA Eligible Emissions Units are to be determined by the ICAO Council, and up-to-date information on eligible units is made available on the ICAO CORSIA website (see question 4.25). |

table-row | 21 | |||||||||||||||||||||||||||||||||||||

| 2.15 | How are an aeroplane operator’s offsetting requirements calculated? |

Paragraph 11 of the Assembly Resolution A41-22 addresses the distribution of the total amount of CO₂ emissions to be offset in a given year among individual aeroplane operators. This is accomplished by introducing a dynamic approach for the distribution of offsetting requirements, which takes into account:

The figure below describes the calculation of an aeroplane operator's offsetting requirements.

|

table-row | 22 | |||||||||||||||||||||||||||||||||||||

| 2.16 | What are CORSIA’s compliance periods? |

Paragraph 15 of the Assembly Resolution A41-22 determines that CORSIA has three-years compliance cycles (also referred to as a compliance period), for which the operators need to reconcile their offsetting requirements. The compliance periods are:

It should be noted that an operator will report its CO₂ emissions on an annual basis, corresponding to calendar years. See question 3.71 for more information on the relationship between CORSIA’s compliance periods and reporting periods. |

table-row | 23 | |||||||||||||||||||||||||||||||||||||

| 2.17 | What are CORSIA’s baseline emissions? |

The ICAO Assembly, having considered the recommendations from the Council arising from the 2022 CORSIA periodic review (see question 2.29), adopted Resolution A41-22, which establishes adjustments to the definition of the CORSIA baseline as follows (Assembly Resolution A41-22, paragraph 11 b)):

|

table-row | 24 | |||||||||||||||||||||||||||||||||||||

| 2.18 | What is the difference between the Sector’s Growth Factor used by the formula under CORSIA and the generally-used term “emissions growth rate”? |

In general, the term “emissions growth rate” refers to the percentage increase in the amount of emissions from the baseline to a given year from 2021, compared to the baseline emissions.

For the purposes of CORSIA, the Sector’s Growth Factor is defined as the percentage increase in the amount of emissions from the baseline to a given year from 2021, compared to the emissions in that given year. |

table-row | 25 | |||||||||||||||||||||||||||||||||||||

| 2.19 | How are CORSIA Eligible Fuels accounted for in the calculation of offsetting requirements? |

From 2021 onwards, operators can reduce their CORSIA offsetting requirements by claiming emissions reductions from CORSIA Eligible Fuels. In order to do this, the operator will:

|

table-row | 26 | |||||||||||||||||||||||||||||||||||||

| 2.20 | Can an aeroplane operator address its offsetting requirements accrued in CORSIA both through CORSIA Eligible Emissions Units and CORSIA Eligible Fuels? |

Yes. For a given compliance period, the operator has the capacity to reduce its total final offsetting requirements by claiming emissions reductions from CORSIA Eligible Fuels (see question 2.19). By doing so, the operator could in principle reduce its total final offsetting requirements to zero, provided that emissions reductions claims are large enough to counter-balance the offsetting requirements accrued in the given compliance period.

If the operator's total final offsetting requirements for a given compliance period have not been reduced to zero through the claiming of emissions reductions from CORSIA Eligible Fuels (either because the operator chooses not to report such claims, or because the reported emissions reductions claims are not large enough), the operator will need to cancel CORSIA Eligible Emissions Units in a quantity equivalent to the value of the total final offsetting requirements for that compliance period (see question 2.14).

Therefore, CORSIA provides operators with two distinct ways of addressing its offsetting requirements in CORSIA. The operator's choice of strategy (use of CORSIA Eligible Fuels; use of CORSIA Eligible Emissions Units; or a combination of both) will be determined on the basis of a variety of factors, including cost considerations related to both CORSIA Eligible Fuels and CORSIA Eligible Emissions Units.

|

table-row | 234 | |||||||||||||||||||||||||||||||||||||

| 2.21 | Can an aeroplane operator’s CO₂ offsetting requirements be negative? |

Compliance periods for offsetting requirements are every 3 years, with the first period starting on 1 January 2021 and ending on 31 December 2023 (see also question 2.16).

If, as a result of the calculation described in questions 2.15 and 2.19, an aeroplane operator’s total final offsetting requirements during a compliance period are negative (e.g., the verified emissions reductions claimed by an operator from the use of CORSIA Eligible Fuels are more than its offsetting requirements), the operator has no offsetting requirements for the compliance period.

Negative offsetting requirements will not be carried forward to a subsequent three-year compliance period. However, if an operator’s offsetting requirements in a given year within a compliance period are negative, the operator reduces its total final offsetting requirement for the three-year compliance period.

|

table-row | 27 | |||||||||||||||||||||||||||||||||||||

| 2.22 | Will an aeroplane operator, which reduces its emissions compared to the baseline, have any offsetting requirements? |

If an operator’s emissions do not increase or decrease compared to the baseline emissions, there will still be offsetting requirements for the operator, as long as the global emissions covered by CORSIA increase above the global baseline emissions (i.e. the Sector’s Growth Factor is positive).

Potential efforts of such an operator to renew its fleet and improve its operational efficiency will not be ignored, as the calculation of CORSIA offsetting requirements for the operator will be done by multiplying the Sector’s Growth Factor with the operator’s emissions covered by CORSIA offsetting requirements in a given year. Such efforts are reflected in the operator’s level of emissions, and offsetting requirements would be smaller than using the operator’s emissions without fleet renewal or operational improvements in the calculation. Therefore, the CORSIA maintains incentives for individual operators to make efforts to improve their fuel efficiency.

The incentive for individual aeroplane operators to reduce their emissions is further strengthened starting from 2033, when an individual aeroplane operator’s Growth Factor will be added to the offsetting requirements calculation formula. The individual Growth Factor represents an individual operator’s Growth Factor of emissions in a given year, and the weight of this factor in the formula of calculating the offsetting requirements has been set to 15 per cent for the years 2033-2035, following the adjustments made by the 41st Session of the ICAO Assembly to the CORSIA design elements, in line with the recommendations by the Council arising from the 2022 CORSIA periodic review. Please see question 2.15 for more information.

|

table-row | 28 | |||||||||||||||||||||||||||||||||||||

| Key design element 4: Exemptions and new entrants | none | ||||||||||||||||||||||||||||||||||||||||

| 2.23 | Does the CORSIA include provisions to exempt very low international aviation activities? |

Paragraph 13 of the Assembly Resolution A41-22 provides the following exemptions from the CORSIA offsetting requirements for the purposes of avoiding an administrative burden from the application of CORSIA due to low levels of international aviation activities:

|

table-row | 29 | |||||||||||||||||||||||||||||||||||||

| 2.24 | How will the CORSIA apply to new operators that will initiate activities after the entry into force of the scheme (a so-called “new entrant”)? |

Paragraph 12 of the Assembly Resolution A41-22 refers to “new entrants” as aeroplane operators that commence an aviation activity falling within the scope of the CORSIA. This paragraph outlines criteria to determine when “new entrants” should start participating in the CORSIA offsetting, with the exemption period being the earliest out of the following two:

In other words, a new entrant is exempted from the application of the CORSIA offsetting requirements for the first 3 years, or until its annual emissions exceed 0.1% of total 2019 emissions from the international aviation sector. The condition that applies earlier will determine when a new entrant’s emissions are subject to the offsetting requirements.

It is important to note that the CO₂ emissions of a new entrant are still to be reported from the year after the new entrant falls under the applicability of CORSIA MRV requirements (also see question 3.19), regardless of the exemptions from the CORSIA offsetting requirements.

In the example below, operators A and B start operations in year 2022 as shown in the table. According to the Assembly Resolution A41-22, operator A will have offsetting requirements starting in 2025, and operator B in 2024. However, both operators will need to comply with the MRV requirements from 2023 onwards, assuming that they are within the CORSIA MRV applicability.

1 The ICAO Assembly, having considered the recommendations from the Council arising from the 2022 CORSIA periodic review (see question 2.28), adopted Resolution A41-22, in which 2019 replaces 2020 for the definition of the new entrant threshold (Assembly Resolution A41-22, paragraph 12).

|

table-row | 32 | |||||||||||||||||||||||||||||||||||||

| 2.25 | Will a new entrant operator affect the CORSIA baseline? |

In line with the amendments to the CORSIA design elements agreed upon by the ICAO Assembly through adoption of Resolution A41-22, only CO₂ emissions corresponding to year 2019 are relevant for the purpose of defining CORSIA's baseline (see question 2.17 for more details on CORSIA's baseline).

The CO₂ emissions of a new entrant are to be reported from the year after the CORSIA MRV system begins to apply to the operator (see question 2.24). This means that the soonest that a new entrant could fall within the applicability of CORSIA MRV requirements would be in 2020. Therefore, any new entrant will not affect the CORSIA baseline, as the new entrant's CO₂ emissions in year 2019 would not be monitored and reported under CORSIA. CAEP work is ongoing to produce recommendations for how to determine individual baseline emissions for new entrant aeroplane operators. |

table-row | 33 | |||||||||||||||||||||||||||||||||||||

| 2.26 | If an aeroplane operator, which (in the past) had domestic operations only, establishes international routes, will it be considered a new entrant? |

According to the guidance provided in the Environmental Technical Manual, Volume IV, for an aeroplane operator to qualify as a new entrant, both the following conditions should be met:

This could be interpreted in a way that an aeroplane operator does not actually need to be a newly created entity. Indeed, the entity can exist since many years without having operated any or a sufficient (in terms of CO₂ emissions on international routes) number of international flights. This would be the case for instance of a well-established aeroplane operator flying only domestic routes and then starting to operate on international routes. |

table-row | 30 | |||||||||||||||||||||||||||||||||||||

| Key design element 5: Review process | none | ||||||||||||||||||||||||||||||||||||||||

| 2.27 | Does the CORSIA include provisions to review its implementation and to make adjustments if needed? |

Paragraph 9 g) of the Assembly Resolution A41-22 includes a provision that the ICAO Council will conduct a review of the implementation of the CORSIA every three years, starting in 2022. This review will include an assessment of the impact of the CORSIA on the growth of international aviation. The results of this assessment will serve as an important basis for the Council to consider adjustments and make recommendations to the Assembly for decisions about the next implementation phase or compliance period, as appropriate.

In addition, as elaborated in paragraph 17 of the Assembly Resolution A41-22 - the purpose of the periodic review is to contribute to the sustainable development of the international aviation sector and to the effectiveness of the scheme. The review will assess, inter alia: the progress towards achieving ICAO’s global aspirational goal, the scheme’s market and cost impact on States and aeroplane operators and on international aviation, and the functioning of the scheme’s design elements. The review will also involve consideration of the scheme’s improvements that would support the purpose of the Paris Agreement or simply result in better design. The Assembly requested the Council to develop a methodology and timeline to conduct such reviews in the future.

A special review will be performed by the end of 2032 regarding the termination of the scheme, its extension or any other post-2035 improvements. The sequence of the phases of the CORSIA, compliance periods, periodic reviews, special review and ICAO Assemblies is summarized in the figure below.  |

table-row | 34 | |||||||||||||||||||||||||||||||||||||

| 2.28 | What was the methodology followed to undertake the 2022 CORSIA periodic review? |

In March 2021, the ICAO Council agreed on the process and Terms of Reference for the 2022 CORSIA periodic review, including a series of requests to CAEP for providing inputs and analyses to support the Council's subsequent work on this topic.

In accordance with the agreed process for the 2022 CORSIA periodic review, a State letter consultation process also took place to collect input from States on their experiences regarding CORSIA implementation (State letter ENV 6/6 –21/33, issued on 7 May 2021). These States' inputs were considered by the Council in the context of its work on the 2022 CORSIA periodic review.

The various inputs provided by CAEP throughout the 2022 CORSIA periodic review were made publicly available in the ICAO CORSIA webpage upon Council's consideration.

|

table-row | 31 | |||||||||||||||||||||||||||||||||||||

| 2.29 | What was the outcome of the 2022 CORSIA periodic review? |

The Council, at its 226th Session in August 2022, finalized its work on the 2022 CORSIA periodic review with the consideration of the requested CAEP inputs.

The Council agreed on its recommendations arising from the 2022 CORSIA periodic review, for consideration by the 41st Session of the ICAO Assembly, including the following adjustments to the CORSIA design features:

|

table-row | 231 | |||||||||||||||||||||||||||||||||||||

| 2.30 | What will be the methodology applied for future CORSIA periodic reviews? |

The 41st Session of the ICAO Assembly requested the Council to develop a methodology and timeline to conduct future CORSIA periodic reviews (paragraph 17 of Assembly Resolution A41-22). The outcome of Council’s work on this matter will be applied at the 2025 CORSIA periodic review and at subsequent reviews.

|

table-row | 232 | |||||||||||||||||||||||||||||||||||||

| 3. | Questions about Annex 16, Volume IV - CORSIA | none | 35 | ||||||||||||||||||||||||||||||||||||||

| General questions related to Annex 16, Volume IV | none | ||||||||||||||||||||||||||||||||||||||||

| 3.1 | What are the differences between: Annex 16, Volume IV; Environmental Technical Manual, Volume IV; and CORSIA Implementation Elements? |

Annex 16, Volume IV and Environmental Technical Manual (ETM), Volume IV follow a similar structure to that of the Annex 16, Volumes I, II and III. This is the traditional ICAO Standards and Recommended Practices (SARPs) approach, where the implementation of the SARPs is supported by guidance material.

The SARPs of Annex 16, Volume IV provide the necessary actions by States or operators (the “what” and “when”) to implement CORSIA, whereas the Environmental Technical Manual (ETM), Volume IV provides the guidance on the process (the “how”) to implement CORSIA.

Due to CORSIA’s specific characteristics, CORSIA Implementation Elements have been developed. The Implementation Elements are reflected in 14 ICAO documents, which are directly referenced in the SARPs and contain essential information for the implementation of CORSIA. These ICAO documents are made available on the ICAO CORSIA website, once approved by the ICAO Council, and may only be amended by the ICAO Council.

The table below provides information on the linkages each of the ICAO CORSIA Implementation Elements and the corresponding ICAO documents. Please refer to section 4 of these FAQs for more information on CORSIA Implementation Elements and corresponding ICAO documents.

|

table-row | 36 | |||||||||||||||||||||||||||||||||||||

| 3.2 | What ICAO process was followed to develop Annex 16, Volume IV? |

Following the adoption of Assembly Resolution A39-3, the ICAO Council in November 2016 endorsed the overall plan of CORSIA preparatory activities on the development of CORSIA-related SARPs and guidance. The Council also established an Advisory Group on CORSIA (AGC) to serve as an advisory body to the Council. CAEP was tasked to develop recommendations for CORSIA-related SARPs and guidance.

Following CAEP’s recommendation, preliminary reviews by the AGC and ICAO’s Air Navigation Commission (ANC), consultation with Member States, and the final reviews by AGC and ANC, the CORSIA-related SARPs were adopted by the Council on 27 June 2018 in the form of the first edition of Annex 16 - Environmental Protection to the Convention on International Civil Aviation, Volume IV — Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA). The first edition of Annex 16, Volume IV became applicable on 1 January 2019.

The Council, at its 228th Session (13 – 31 March 2023), adopted Amendment 1 to Annex 16, Volume IV, resulting from proposed amendments by CAEP and from the outcome of the 2022 CORSIA periodic review, and having undertaken preliminary and final reviews by ANC and consultation with Member States. The resulting second edition of Annex 16, Volume IV became applicable on 1 January 2024.

|

table-row | 37 | |||||||||||||||||||||||||||||||||||||

| Administrative aspects | none | ||||||||||||||||||||||||||||||||||||||||

| 3.3 | What is the definition of international flight for CORSIA purposes? |

Reference in Annex 16, Volume IV: Part II, Chapter 1, 1.1.2.

For the purposes of CORSIA, an international flight is defined as the operation of an aircraft from take-off at an aerodrome of a State or its territories, and landing at an aerodrome of another State or its territories.

|

table-row | 38 | |||||||||||||||||||||||||||||||||||||

| 3.4 | What guidance should be followed to determine whether a flight is international or domestic? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.1.2.

For the purposes of CORSIA, an international flight is defined as the operation of an aircraft from take-off at an aerodrome of a State or its territories, and landing at an aerodrome of another State or its territories (see also question 3.3).

When considering whether a flight is international or domestic for the purposes of CORSIA, an aeroplane operator and a State should use Doc 7910 — Location Indicators, which contains a list of aerodromes and the State they are attributed to.

|

table-row | 141 | |||||||||||||||||||||||||||||||||||||

| 3.5 | Does CORSIA apply to international flights to/from non-ICAO States? |

Reference: Environmental Technical Manual, Volume IV, Chapter 2, 2.1.1

CORSIA is implemented through Annex 16, Volume IV to the Convention on International Civil Aviation (Chicago Convention), which applies to Contracting States of the Convention. Flights taking off from or landing at an aerodrome of a State, or one of its territories, which is not an ICAO Member State are not considered to fall within the applicability scope of Annex 16, Volume IV.

|

table-row | 142 | |||||||||||||||||||||||||||||||||||||

| 3.6 | What is the definition of an "aeroplane" in CORSIA? How does this definition differ from the definition of an “aircraft”? |

Reference in Annex 16, Volume IV: Part I, Chapter 1, Definitions.

The following definition of “an aeroplane” is included in the Annex 16, Volume IV: Aeroplane. A power-driven heavier-than-air aircraft, deriving its lift in flight chiefly from aerodynamic reactions on surfaces which remain fixed under given conditions of flight.

Regarding the difference between the definitions of an aircraft and an aeroplane, Annex 2 to the Convention on International Civil Aviation offers the following definition for “an aircraft”:

Aircraft. Any machine that can derive support in the atmosphere from the reactions of the air other than the reactions of the air against the earth’s surface.

Under CORSIA, only aeroplane operators will have compliance requirements (see also question 3.26).

|

table-row | 143 | |||||||||||||||||||||||||||||||||||||

| 3.7 | What is the definition of “an aerodrome” in CORSIA? |

Reference in Annex 16, Volume IV: Part I, Chapter 1, Definitions.

Annex 16, Volume IV offers the following definition for “an aerodrome”: Aerodrome. A defined area on land or water (including any buildings, installations and equipment) intended to be used either wholly or in part for the arrival, departure and surface movement of aircraft.

|

table-row | 144 | |||||||||||||||||||||||||||||||||||||

| 3.8 | How are diverted flights handled in CORSIA? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.1.

Diversion of flights can lead to any of the following scenarios:

a) A flight originally subject to MRV requirements, which continues to be subject to such requirements as a result of the diversion; b) A flight originally not subject to MRV requirements, which continues not to be subject to such requirements as a result of the diversion; c) A flight originally subject to MRV requirements, which is no longer subject to such requirements as a result of the diversion; or d) A flight originally not subject to MRV requirements, which is no longer subject to such requirements as a result of the diversion.

Under CORSIA, in any of the scenarios listed above, the actual aerodromes of departure and arrival for a flight, rather than the scheduled ones, will be taken as a reference to determine whether or not that flight is subject to MRV requirements. See also question 3.31.

|

table-row | 39 | |||||||||||||||||||||||||||||||||||||

| 3.9 | What does a “State pair” mean? Is it uni- or bidirectional? |

Reference in Annex 16, Volume IV: Part I, Chapter 1 – Definitions.

In CORSIA, State pair is being defined as a group of two States composed of a departing State or its territories and an arrival State or its territories. For example, when reporting CO₂ emissions from international flights between States A and B, an aeroplane operator will report both directions as separate State pairs (A-B and B-A).

|

table-row | 40 | |||||||||||||||||||||||||||||||||||||

| 3.10 | Who will ensure that aeroplane operators comply with the requirements of Annex 16, Volume IV? |

Reference in Annex 16, Volume IV: Part II, Chapter 1, 1.3.1.

According to Assembly Resolution A41-22, paragraph 19 f), ICAO Member States will take necessary action to ensure that the national policies and regulatory framework be established for the compliance and enforcement of CORSIA.

As per Annex 16, Volume IV, an aeroplane operator will be attributed to a State for administering CORSIA based on the rules for attribution (see question 3.12). The State is primarily responsible for ensuring that the aeroplane operator complies with the CORSIA requirements.

|

table-row | 41 | |||||||||||||||||||||||||||||||||||||

| 3.11 | How is an international flight being attributed to a single aeroplane operator? |

Reference in Annex 16, Volume IV: Part II, Chapter 1, 1.1.3.

It is important to identify all applicable international flights so that the CO₂ emissions from these flights are monitored and reported. Also, each international flight should be allocated to a single aeroplane operator. In order to achieve this, the following information will be used for attributing international flights to an aeroplane operator:

|

table-row | 42 | |||||||||||||||||||||||||||||||||||||

| 3.12 | How is an aeroplane operator being attributed to a single State? |

Reference in Annex 16, Volume IV: Part II, Chapter 1, 1.2.

Under CORSIA, each aeroplane operator will report its CO₂ emissions to a single State. The rules for attributing an aeroplane operator to a State are based on:

The State is required to ensure the correct attribution of an aeroplane operator to it. In order to determine which aeroplane operators fall under its administration, the State should take the following steps: review operators' possible communications indicating that are likely to be administered by the State, review the contents of Doc 8585 — Designators for Aircraft Operating Agencies, Aeronautical Authorities and Services, and identify those operators that are notified by the State, review AOCs issued by that State, and review of registered entities within that particular State (e.g., from the State's company register).

It should be noted that the "place of juridical registration" refers to the State in which the entity (company or person) is legally registered. The purpose is to have jurisdictional clarity in cases of enforcement, such as international court measures. The place of juridical registration may differ from the principal place of business.

Regarding the use of the expression "AOC (or equivalent)", the wording "or equivalent" is used because in some States the AOC is named differently. The "AOC" refers to an official document issued by a State that gives an aeroplane operator license to operate and that contains the identification of the aircraft operator and may also contain aircraft registration marks. The use of general aviation operating certificates and other certificates permitting non-commercial air transport could thus be appropriate as long as these certificates are issued/approved by a State.

After identifying the aeroplane operators under its administration, the State is required to submit to ICAO information of those aeroplane operators that are attributed to it, and ICAO will publish a list of aeroplane operators and the States attributions on the ICAO CORSIA website, as a part of the ICAO document entitled "CORSIA Central Registry (CCR): Information and Data for Transparency".

|

table-row | 43 | |||||||||||||||||||||||||||||||||||||

| 3.13 | Can an aeroplane operator delegate its administrative requirements? |

Reference in Annex 16, Volume IV: Part II, Chapter 1, 1.1.5.

Yes, an aeroplane operator can delegate its CORSIA administrative requirements to a third party. However, this third party cannot be the same entity as the verification body. Also, liability for compliance with the CORSIA requirements will remain with the aeroplane operator.

|

table-row | 44 | |||||||||||||||||||||||||||||||||||||

| 3.14 | Can an aeroplane operator report together with one or more of its subsidiaries? |

Reference in Annex 16, Volume IV: Part II, Chapter 1, 1.2.6.

An aeroplane operator can report together with a subsidiary company, if the subsidiary is:

If two aeroplane operators are treated as a single consolidated aeroplane operator, the two operators will be administered as a single entity, and their emissions aggregated. Therefore, the applicability of the requirements of Annex 16, Volume IV will be based on their aggregated emissions.

|

table-row | 45 | |||||||||||||||||||||||||||||||||||||

| 3.15 | Who is responsible for reporting emissions from flights operated with leased aeroplanes? |

Reference in Annex 16, Volume IV: Part II, Chapter 1, 1.1.2.

According to Annex 16, Volume IV, the attribution of international flights to an operator is based on the Flight Plan, Item 7, which means that the operating entity (i.e. in a case of wet-lease arrangement, the lessee) is responsible for the international flights (under the lessee’s ICAO Designator) and therefore responsible for compliance of the international flights attributed to the lessee.

In addition, the State of the lessee is responsible for administrative tasks related to lessee, for example approval of the lessee’s Emissions Monitoring Plan and Emissions Report.

|

table-row | 145 | |||||||||||||||||||||||||||||||||||||

| 3.16 | Can a State delegate its administration processes under the CORSIA to another State? |

Reference in Annex 16, Volume IV: Part II, Chapter 1, 1.3.2.

Yes, a State may delegate administration processes of CORSIA to another State through an administrative partnership based on a bilateral agreement between the respective States. Nevertheless, the State shall not delegate enforcement of CORSIA requirements, or its administrative tasks towards ICAO, to another State.

If such an arrangement is agreed upon, the State receiving capacity support must ensure that aeroplane operators attributed to that State are advised of the administrative arrangements.

|

table-row | 46 | |||||||||||||||||||||||||||||||||||||

| 3.17 | How long does a State and an aeroplane operator need to keep CORSIA-related records? What is included in those records? |

Reference in Annex 16, Volume IV: Part II, Chapter 1, 1.4, and Appendix 4.

An aeroplane operator is required to keep records relevant to demonstrating compliance with the requirements of Chapters 2, 3, and 4 of Annex 16, Volume IV, Part II, for a period of 10 years. It is also recommended that an aeroplane operator keep records relevant to its CO₂ emissions per State pair during the 2019-2020 period in order to allow the operator to cross-check its offsetting requirements calculated by the State during the 2030-2035 compliance periods.

An operator is required to include a documentation and record keeping plan in its Emissions Monitoring Plan for the approval by the State. This plan will specify how (e.g., by using an IT system), and where the operator will store CORSIA-relevant information.

The State shall keep records relevant to the aeroplane operator's CO₂ emissions per State pair during the period of 2019-2020 in order to calculate the aeroplane operator's offsetting requirements during the 2030-2035 compliance periods.

|

table-row | 47 | |||||||||||||||||||||||||||||||||||||

| Monitoring, reporting and verification (MRV) | none | ||||||||||||||||||||||||||||||||||||||||

| 3.18 | What are the components of the CORSIA MRV system? |

Reference in Annex 16, Volume IV: Part II, Chapter 2.

CORSIA’s MRV (Monitoring, Reporting and Verification) system consists of three components:

|

table-row | 48 | |||||||||||||||||||||||||||||||||||||

| 3.19 | What is the applicability of the CORSIA MRV requirements? Are they any exemptions? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.1.

All aeroplane operators conducting international flights are required to monitor, report and verify CO₂ emissions from these flights from 1 January 2019 until 31 December 2035. It should be noted that the requirement for the MRV of CO₂ emissions is independent from participation in CORSIA offsetting.

As per Annex 16, Volume IV, the MRV requirements do not apply to:

|

table-row | 49 | |||||||||||||||||||||||||||||||||||||

| 3.20 | In view of the decisions made by the ICAO Council in order to safeguard against inappropriate economic burden on aeroplane operators due to the COVID-19 pandemic, did aeroplane operators have to undertake the monitoring, reporting and verification of CO₂ emissions from international flights operated in 2020? |

The decisions made by the Council at its 220th Session did not bring a change to the provisions of Annex 16, Volume IV or to the then-applicable Assembly Resolution A40-19.

Consequently, the monitoring, reporting and verification of CO₂ emissions from international flights operated in 2020 had to be undertaken as per the requirements in Annex 16, Volume IV.

|

table-row | 50 | |||||||||||||||||||||||||||||||||||||

| 3.21 | Can an aeroplane operator with emissions of less than 10 000 tonnes of CO₂ per year be included in CORSIA? |

Reference in Annex 16, Volume IV: Part II, Chapter 1, 1.2.6, Chapter 2, 2.1.

An aeroplane operator that produces annual CO₂ emissions from international flights less than or equal to 10 000 tonnes is not subject to the requirements of Annex 16, Volume IV (see also question 3.19).

However, if an aeroplane operator below the threshold of 10 000 tonnes of CO₂ is wholly-owned by and legally registered in the same State as another aeroplane operator, the two aeroplane operators can request to be treated as a single operator (see question 3.14). In this case the combined emissions of both aeroplane operators could exceed this threshold and become subject to the applicability of the MRV requirements of CORSIA.

|

table-row | 132 | |||||||||||||||||||||||||||||||||||||

| 3.22 | What are the actions for an aeroplane operator, who has been covered by CORSIA, but now drops below the 10 000 tonnes of CO₂ threshold? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.1.

If an aeroplane operator falls below the 10 000 tonnes threshold in a given year, then it falls outside the scope of applicability of Annex 16, Volume IV and would not have any requirements in that year. In such an instance, it is suggested the aeroplane operator contact its State of attribution to inform them that they are below the threshold. The State may choose to engage with the operator to confirm that the aeroplane operator is out of the scope of applicability.

|

table-row | 147 | |||||||||||||||||||||||||||||||||||||

| 3.23 | How to address aeroplane operators with annual CO₂ emissions close to the 10 000 tonnes threshold? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.1.

If an aeroplane operator is close to the 10 000 tonnes threshold of annual CO₂ emissions, it should consider engaging with the State for guidance. Likewise, the State should carry out oversight of the aeroplane operators attributed to it, and engage with any that it considers may be close to or above the threshold. The aeroplane operator with annual CO₂ emissions below the threshold may also choose to voluntarily engage with the State to which it is attributed (e.g. to declare that the operator’s emissions are below the threshold).

|

table-row | 51 | |||||||||||||||||||||||||||||||||||||

| 3.24 | Are aeroplane manufacturers or airports subject to any requirements under Annex 16, Volume IV? |

No, aeroplane manufacturers and airports do not have requirements under Annex 16, Volume IV, unless those entities operate international flights themselves, and thus become aeroplane operators as defined in Annex 16, Volume IV.

|

table-row | 52 | |||||||||||||||||||||||||||||||||||||

| 3.25 | Is a re-positioning flight before or after an exempted humanitarian, medical or firefighting flight exempt? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.1.

Yes. Flights preceding or following humanitarian, medical or firefighting flights are also exempt if they were required to accomplish the humanitarian, medical or firefighting activities or to reposition the aeroplane thereafter. The operator will have to be able to provide evidence of the nature of the flight. See also question 3.19. |

table-row | 53 | |||||||||||||||||||||||||||||||||||||

| 3.26 | Are helicopter operations covered by the CORSIA MRV system? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.1.

No. The applicability of the CORSIA MRV requirements covers aeroplanes, and helicopter operations are outside of the scope of applicability of CORSIA. See also question 3.6. |

table-row | 54 | |||||||||||||||||||||||||||||||||||||

| 3.27 | Are international flights by police, military, customs or State aircraft within the scope of applicability of the CORSIA MRV system? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.1.

No, Annex 16, Volume IV only applies to international civil aviation; international flights from police, military, customs and State aircraft are excluded from the Chicago Convention as per Article 3, and thus are excluded from the scope of CORSIA. |

table-row | 148 | |||||||||||||||||||||||||||||||||||||

| 3.28 | How can humanitarian, medical, firefighting, police, military, customs and State aircraft flights be identified? |

Reference: Environmental Technical Manual, Volume IV, Chapter 2, 2.1.4.

An aeroplane operator should provide evidence to the State to which it has been attributed to prove that an operation was a humanitarian, medical, firefighting, military or State aeroplane flight. Information included in Item 8 (flight rules and type of flight) of the flight plan can be used to demonstrate the nature of a flight, and the ETM, Volume IV provides examples of specific marks that can be included in the Flight Plan in this regard, as per Doc 4444 — Procedures for Air Navigation Services — Air Traffic Management. It should be noted that a State might have in place specific procedures and practices to demonstrate humanitarian, medical, firefighting, police, military, customs and State aircraft flights. The decision to interpret whether a flight is under the applicability of Annex 16, Volume IV is on the State Authority. Procedures for identifying international flights that are exempted from CORSIA’s applicability should be provided within the Emissions Monitoring Plan approved by the State Authority. |

table-row | 149 | |||||||||||||||||||||||||||||||||||||

| 3.29 | Are Search and Rescue (SAR) flights exempted from CORSIA? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.2.5.

|

table-row | 133 | |||||||||||||||||||||||||||||||||||||

| 3.30 | Are repatriation flights operated under specific situations (e.g. COVID-19 pandemic) identified as humanitarian flights in the context of CORSIA implementation? |

The Standards and Recommended Practices in Annex 16, Volume IV do not address the question of defining humanitarian, medical and firefighting flights, but rather the treatment to which these types of flights are subject under CORSIA, as reflected in Annex 16, Volume IV, Part II, Chapter 2, 2.1.1 and 2.1.3.

On the matter of identifying humanitarian, medical and firefighting flights, the following has to be noted:

Therefore, it corresponds to the aeroplane operator to identify a given flight as humanitarian, medical or firefighting, and to provide evidence to the State to prove that such qualification is correct, in line with the established provisions relating to flight plans. If the State considers that such qualification is correct, then the provisions of Annex 16, Volume IV related to humanitarian, medical and firefighting flights will apply.

|

table-row | 55 | |||||||||||||||||||||||||||||||||||||

| 3.31 | How are diversions handled in CORSIA? |

Reference in Annex 16, Volume IV: Part II, Chapter 1, 1.1.2; Chapter 2, 2.1; Chapter 2, 2.2.1.3.3.

A flight should be considered to be diverted when it makes an unplanned landing at an aerodrome different from the destination aerodrome indicated by the aeroplane operator in the last approved flight plan filed prior to the flight departure.

A diverted flight and the subsequent flight are to be treated as two consecutive and separate flights operating, respectively, to and from the aerodrome the diverted flight actually landed at, rather than that which was originally planned.

A diversion is by its nature unplanned. However, according to the rules of CORSIA, whether a flight is international, or subject to offsetting requirements, is based on where it actually went, not where it meant to go.

If in a given year an aeroplane operator is subject to the CORSIA offsetting requirements only because of diverted or subsequent flights (all other flights being operated on routes not subject to offsetting), the aeroplane operator will still be required to offset the emissions of those flights.

Should an aeroplane operator that is approved to use the ICAO CORSIA CERT exceed in a given year the threshold of 50 000 tonnes of CO₂ on the routes subject to offsetting requirements due to diverted or subsequent flights, then the operator will still be permitted to use the ICAO CORSIA CERT in that year and the following year (year y+1). However, if the operator also exceeds the 50 000 tonnes threshold in that following year (year y+1), then it would be required to submit a new Emissions Monitoring Plan by 30th September in (Year y+2) and begin using a Fuel Use Monitoring Method from 1st January in Year y+3.

|

table-row | 56 | |||||||||||||||||||||||||||||||||||||

| Emissions Monitoring Plan | none | ||||||||||||||||||||||||||||||||||||||||

| 3.32 | What is an Emissions Monitoring Plan and why is it needed? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.2.2 and Appendix 4.

An aeroplane operator falling under the applicability of CORSIA MRV requirements is required to submit an Emissions Monitoring Plan to the State Authority for approval. An Emissions Monitoring Plan is a collaborative tool between the State and the aeroplane operator that identifies the most appropriate means and methods for CO₂ emissions monitoring on an operator-specific basis, and also facilitates the reporting of required information to the State. During the development and approval process of the Emissions Monitoring Plan, the State Authority and aeroplane operator should maintain clear and open communication. Working collaboratively for CORSIA preparation and implementation reduces potential errors and increases effectiveness of the CO₂ emissions monitoring. |

table-row | 57 | |||||||||||||||||||||||||||||||||||||

| 3.33 | What are the contents of an Emissions Monitoring Plan? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.2.2 and Appendix 4.

|

table-row | 58 | |||||||||||||||||||||||||||||||||||||

| 3.34 | Is there a standardised template for an Emissions Monitoring Plan? |

A template for an Emissions Monitoring Plan is provided in the Environmental Technical Manual (Doc 9501), Volume IV – Procedures for demonstrating compliance with the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA).

The template is also available on the ICAO CORSIA webpage. |

table-row | 59 | |||||||||||||||||||||||||||||||||||||

| 3.35 | When should an aeroplane operator submit an Emissions Monitoring Plan to the State? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.2.2 and Appendix 1.

In line with the provisions in Annex 16, Volume IV, aeroplane operators that fell within the scope of applicability of MRV requirements at the time when these became applicable (i.e. 1 January 2019) were required to submit their Emissions Monitoring Plan to their State for approval by 28 February 2019. A new entrant aeroplane operator shall submit an Emissions Monitoring Plan to the State to which it is attributed within three months of falling within the scope of applicability of MRV requirements.

An aeroplane operator that falls within the scope of applicability of MRV requirements after 1 January 2021 for the first time without qualifying as a new entrant shall submit an Emissions Monitoring Plan within three months of falling within the scope of applicability.

|

table-row | 60 | |||||||||||||||||||||||||||||||||||||

| 3.36 | When will the Emissions Monitoring Plan be approved by the State? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.2.2 and Appendix 1.

After receiving the Emissions Monitoring Plan from the aeroplane operator, the State Authority will review the plan. If the plan meets the requirements of Annex 16, Volume IV, then the State Authority will approve the Emissions Monitoring Plan. Guidance for the review and approval of an Emissions Monitoring Plan is included in the Environmental Technical Manual (Doc 9501), Volume IV – Procedures for demonstrating compliance with the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA).

|

table-row | 61 | |||||||||||||||||||||||||||||||||||||

| 3.37 | Does the third-party verification body need to review the Emission Monitoring Plan prior to its review and approval by the State? |

Reference in Annex 16, Volume IV: Part I, Chapter 2, 2.2.2.

No. An Emissions Monitoring Plan is a tool to facilitate CORSIA-related communication between an aeroplane operator and a State Authority, and it does not need to be verified by a third-party verification body. A verification body is required to conduct the verification of an Emissions Report that the aeroplane operator develops in accordance with the approved Emissions Monitoring Plan. |

table-row | 62 | |||||||||||||||||||||||||||||||||||||

| 3.38 | Does the Emissions Monitoring Plan have to be submitted annually? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.2.2.

No. The Emissions Monitoring Plan has to be submitted only once unless there are material changes to the operator’s procedures in which case the operator will have to re-submit the Emissions Monitoring Plan to the State Authority for approval. |

table-row | 63 | |||||||||||||||||||||||||||||||||||||

| 3.39 | What happens if there are changes to the information contained in an Emissions Monitoring Plan? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.2.2.

In general, an Emissions Monitoring Plan should reflect the current status of an aeroplane operator’s operations. An operator is required to resubmit the Plan for review and approval by the State if a “material change” is made to the information contained within the Plan. Examples of a material change include:

The aeroplane operator is also required to inform the State of changes that would affect the State’s oversight. This applies even if the changes do not fall within the definition of a material change. Examples of such changes include a change in corporate name or address, or a change in the contact information for a person responsible for the operator’s Emissions Monitoring Plan.

Guidance on identifying material changes to an Emissions Monitoring Plan is provided in the Environmental Technical Manual (Doc 9501), Volume IV – Procedures for demonstrating compliance with the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA).

|

table-row | 150 | |||||||||||||||||||||||||||||||||||||

| 3.40 | How should non-material changes to an Emissions Monitoring Plan be communicated to the State? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.2.2.

An aeroplane operator is required to inform the State of changes that would affect the State’s oversight, including changes that do not fall within the definition of a material change (see question 3.39). As per Annex 16, Volume IV, the operator shall include as a part of its Emissions Monitoring Plan the procedures for providing notice in the Emissions Report of non-material changes that require the attention of the State. Guidance on identifying material and non-material changes to an Emissions Monitoring Plan is provided in the Environmental Technical Manual (Doc 9501), Volume IV – Procedures for demonstrating compliance with the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA). |

table-row | 64 | |||||||||||||||||||||||||||||||||||||

| Monitoring | none | ||||||||||||||||||||||||||||||||||||||||

| 3.41 | How does an aeroplane operator monitor its fuel use and CO₂ emissions? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.2.2. Appendix 2, and Appendix 3.

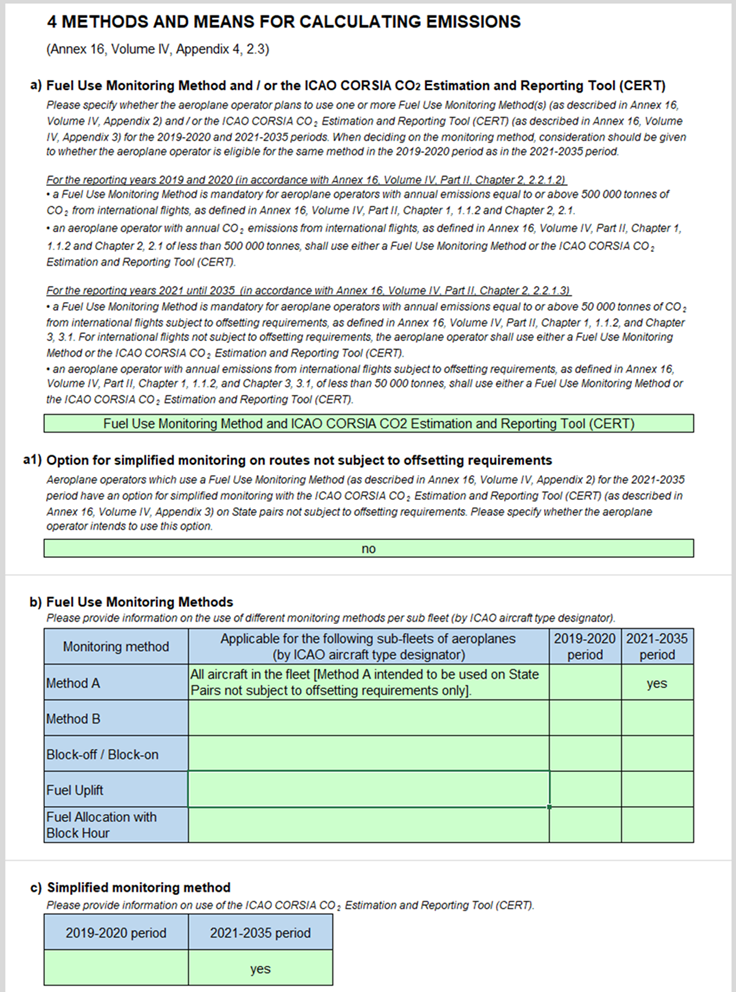

Under CORSIA, there are two possible ways of monitoring the CO₂ emissions: either by tracking the fuel use by applying one of the five Fuel Use Monitoring Methods and then calculating CO₂ emissions from the fuel use, or by using the ICAO CORSIA CO₂ Estimation and Reporting Tool (CERT). Aeroplane operator’s level of activity (see below for the activity thresholds) will determine whether the operator is eligible to use the ICAO CORSIA CERT, or it is required to apply a Fuel Use Monitoring Method. An aeroplane operator will select an appropriate method and include the selection in its Emissions Monitoring Plan, for submission to the State for approval.

An aeroplane operator with annual CO₂ emissions from international flights of less than 500 000 tonnes during the period of 2019-2020 can use the ICAO CORSIA CERT for estimating and reporting its CO₂ emissions under CORSIA (see question 3.43 for more information about the ICAO CORSIA CERT).

An aeroplane operator with annual CO₂ emissions from international flights of more than or equal to 500 000 tonnes during the period of 2019-2020 is required to choose one of the five eligible “Fuel Use Monitoring Methods”. The five Eligible Fuel Use Methods are described more in details in Annex 16, Volume IV, Appendix 2 (see also question 3.46).

For the period of 2021-2035, the eligibility threshold for the use of the ICAO CORSIA CERT changes. For this period, an aeroplane operator can use ICAO CORSIA CERT to estimate and report its annual CO₂ emissions, if the operator’s emissions from international flights subject to offsetting requirements are less than 50 000 tonnes. Also, an operator can still use the ICAO CORSIA CERT to estimate and report those CO₂ emissions from international flights not covered by offsetting requirements.

|

table-row | 151 | |||||||||||||||||||||||||||||||||||||

| 3.42 | Who approves the monitoring method for an aeroplane operator? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.2.1.

An aeroplane operator shall monitor and record its fuel use from international flights in accordance with an eligible monitoring method, and as approved by the State to which it is attributed. It is the responsibility of the State to approve an appropriate monitoring method for an operator, as a part of the approval of the operator’s Emissions Monitoring Plan. |

table-row | 152 | |||||||||||||||||||||||||||||||||||||

| 3.43 | Who are eligible to use the ICAO CORSIA CO₂ Estimation and Reporting Tool (CERT)? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.2.2, and Appendix 3.

Assembly Resolution A39-3 requested the development of simplified MRV procedures as a part of the CORSIA MRV system. ICAO CORSIA CERT is a simplified tool that is designed to help aeroplane operators to estimate and report their international aviation emissions. All aeroplane operators can use the ICAO CORSIA CERT for a preliminary CO₂ assessment to support the determination of an appropriate eligible method for the monitoring of the CO₂ emissions. Eligible aeroplane operators can use ICAO CORSIA CERT for estimating and reporting of their annual CO₂ emissions (see question 3.41 for the eligibility criteria for using the ICAO CORSIA CERT). |

table-row | 66 | |||||||||||||||||||||||||||||||||||||

| 3.44 | Where can one access the ICAO CORSIA CERT? |

ICAO CORSIA CERT is available free of charge on the ICAO CORSIA webpage.

|

table-row | 153 | |||||||||||||||||||||||||||||||||||||

| 3.45 | Where can one find more information about ICAO CORSIA CERT? |

The ICAO CORSIA webpage contains detailed information on the ICAO CORSIA CERT, namely: a document containing technical details on the development and use of the ICAO CORSIA CERT; a Frequently Asked Questions document; and a tutorial.

Please also refer to section 4 of these FAQs for more information on ICAO CORSIA CERT. |

table-row | 67 | |||||||||||||||||||||||||||||||||||||

| 3.46 | What are the five eligible Fuel Use Monitoring Methods? Are they different from ICAO CORSIA CERT? |

Reference in Annex 16, Volume IV: Part II, Chapter 2, 2.2.2, and Appendix 2.

Not all aeroplane operators are eligible to use the ICAO CORSIA CERT for estimating and reporting their annual CO₂ emissions (see question 3.41). Operators which are ineligible to use the ICAO CORSIA CERT shall select and use one of the five eligible Fuel Use Monitoring Methods.

The five methods are entitled as “Method A”; “Method B”; “Block-off / Block-on”; “Fuel Uplift”; and “Fuel Allocation with Block Hour”, and are described in details in Annex 16, Volume IV, Appendix 2, as well as in the Environmental Technical Manual (Doc 9501), Volume IV - Procedures for demonstrating compliance with the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA). These five methods represent the most accurate established practices and are equivalent (i.e. there is no hierarchy for selecting one method). Providing five methods allows for flexibility for the operator to choose a method that best fits its existing fuel use tracking procedures.

The differences in results between the five Fuel Use Monitoring Methods are not significant, in particular over a full reporting period. A comparison of the methods performed by CAEP experts demonstrated that there are no major differences between the results of the methods for the purpose of CORSIA. An aeroplane operator can use a different Fuel Use Monitoring Method for different aeroplane types included in its fleet.

The aeroplane operator is required to specify in its Emissions Monitoring Plan which method it will apply to which aeroplane type. Aeroplane types are included in Doc 8643 — Aircraft Type Designators (https://www.icao.int/publications/DOC8643/Pages/Search.aspx).